Saving tax and building wealth are not always the same goal, but the right instrument can do both. Section 80C of the Income Tax Act, 1961 allows individuals to claim deductions of up to ₹1.5 lakh per financial year, and three instruments come up in almost every conversation about it: ELSS vs PPF vs NPS. Each one works differently. One gives you equity-linked growth with a short lock-in, another offers government-backed safety with full tax exemption, and the third is designed to build retirement income. Knowing how they compare on returns, risk, lock-in, and tax treatment helps you make a choice that goes beyond just saving tax in March.

What Is ELSS?

An ELSS fund invests the majority of its corpus in equity-based securities, typically 80% or higher. The tax-saving investment options under Section 80C provide three different investment periods. The returns which depend on market performance will exceed traditional savings instruments after a long investment duration. You can invest in ELSS via lump sum or regular SIP instalments starting from ₹500. The fund provides two different investment paths for investors to select between growth and dividend options which trained professionals handle.

Tax benefits of ELSS:

- You can claim deductions up to ₹1.5 lakh per financial year under Section 80C through ELSS.

- When you withdraw, returns are classified as LTCG.Profits earnings beyond ₹1.25 lakh attract 12.5% tax under LTCG rules, gains up to ₹1.25 lakh remain exempt.

- ELSS follows an EET structure, contributions and growth are exempt, and returns are taxed only at redemption above the ₹1.25 lakh threshold.

What Is PPF?

PPF is a government-supported savings scheme with a maturity period of 15 years. The scheme allows deposits starting from ₹500 up to ₹1.5 lakh per year. Contributions are eligible for tax benefits within the 80C limit.

Loan access starts in year 3, while withdrawal begins in year 7. After maturity, the account can be extended for any number of blocks of 5 years with or without further deposits. The account can remain active without further contributions after maturity, with the prevailing rate of interest continuing to apply.

PPF is one of the few instruments in India that offers complete safety of capital along with tax-free returns. Being government-guaranteed, it carries virtually no credit risk. The interest rate, currently 7.1% per annum compounded annually, is declared by the government every quarter. While the rate is subject to revision, it has historically remained competitive against inflation over the long term. It is a scalable option for investors seeking stability without being prone to market fluctuations.

Tax benefits of PPF:

- The deposits to the scheme are eligible to avail for deductions under Section 80C up to ₹1.5 lakh.

- Returns generated are completely tax-free annually.

- The entire maturity corpus is tax-free at the end of the 15-year period.

- Limited withdrawals become available after seven years of holding and are also tax-free.

- PPF enjoys full EEE (Exempt-Exempt-Exempt) status, no tax is payable at any stage, whether on contribution, interest, or maturity.

What Is NPS?

NPS is a contributory periodic plan by the Central Government designed to provide retirement income.

The system is governed by PFRDA under the 2013 regulatory act. The scheme is simple, voluntary, portable, and flexible, and is available to all citizens of India between the age of 18 and 85 years.

NPS is structured into two tiers. The Tier-I account acts as the primary retirement corpus where contributions from both employee and employer are invested as per selected funds and managers.

Tier-II is an non-mandatory savings account that allows withdrawals and is available only if a Tier-I account exists. Investors can distribute funds across equity, corporate debt, government securities, and alternative investment categories.

NPS can adjust your investment mix depending on how much risk you are willing to take and returns you expect. You are also permitted to change their pension fund manager and adjust scheme preferences when needed. NPS offers seamless portability across jobs, sectors, and locations, making it particularly suitable for professionals who change employers over the course of their careers.

What sets NPS apart from ELSS and PPF is its purpose. It is not a general savings or investment instrument, it is a retirement vehicle. The corpus built in NPS is structured to provide income after retirement, not a lump sum to deploy elsewhere. This distinction matters when choosing where to allocate funds.

Tax benefits of NPS:

- Tax deduction up to 10% of salary (Basic + DA) under Section 80CCD(1), within the overall ceiling of ₹1.50 lakh under Section 80CCE.

- An extra deduction of ₹50,000 is available under Section 80CCD(1B), beyond the standard 80C ceiling, making NPS unique for additional tax savings. Making NPS the only instrument that allows tax savings beyond the Section 80C limit.

- Contributions made by employers qualify for tax benefits up to 10–14% of salary depending on the tax regime in accordance with Section 80CCD(2).

- 60% of the accumulated corpus withdrawn at retirement is fully exempt from tax under Section 10(12A). The balance 40% goes into an annuity plan, with taxation applicable on periodic income received subsequently is taxable as per the applicable slab.

ELSS vs PPF vs NPS: Full Comparison

When comparing ELSS vs PPF vs NPS, all three qualify for tax deductions under Section 80C, but that is where the similarities end. These investment options vary widely in terms of risk exposure, returns, lock-in duration, and financial objectives.

| Parameter | ELSS | PPF | NPS |

| Primary purpose | Wealth creation + tax saving | Safe long-term savings | Retirement-focused wealth building |

| Nature of investment | Equity market-linked fund | Fixed-income government scheme | Hybrid (equity + debt, investor-controlled) |

| Lock-in flexibility | Shortest (3 years) | Very long (15 years) | Locked till retirement (age 60) |

| Return possibility | High (but volatile) | Stable and predictable | Moderate to high (depends on allocation) |

| Capital safety | No guarantee | Fully guaranteed by government | Partially market-dependent |

| Ideal investment timeline | 5–10 years | 15+ years | 20–30 years (retirement horizon) |

| Liquidity access | Moderate (after 3 years) | Low (restricted withdrawals) | Very low (strict withdrawal rules) |

| Tax benefit (core) | Up to ₹1.5L under 80C | Up to ₹1.5L under 80C | Up to ₹1.5L under 80CCD(1) |

| Extra tax advantage | None | None | Additional ₹50,000 under 80CCD(1B) |

| Tax efficiency (maturity) | Partially taxable (LTCG rules apply) | Fully tax-free (EEE) | Partially tax-efficient (mixed taxation) |

| Risk level | High | Very low | Customisable (low to high) |

| Investor control | No control over stock selection | No control | High control over asset allocation |

| Best for investor type | Growth-oriented investors | Conservative, risk-averse investors | Salaried + retirement planners |

| Wealth vs income focus | Wealth growth | Capital protection | Retirement income generation |

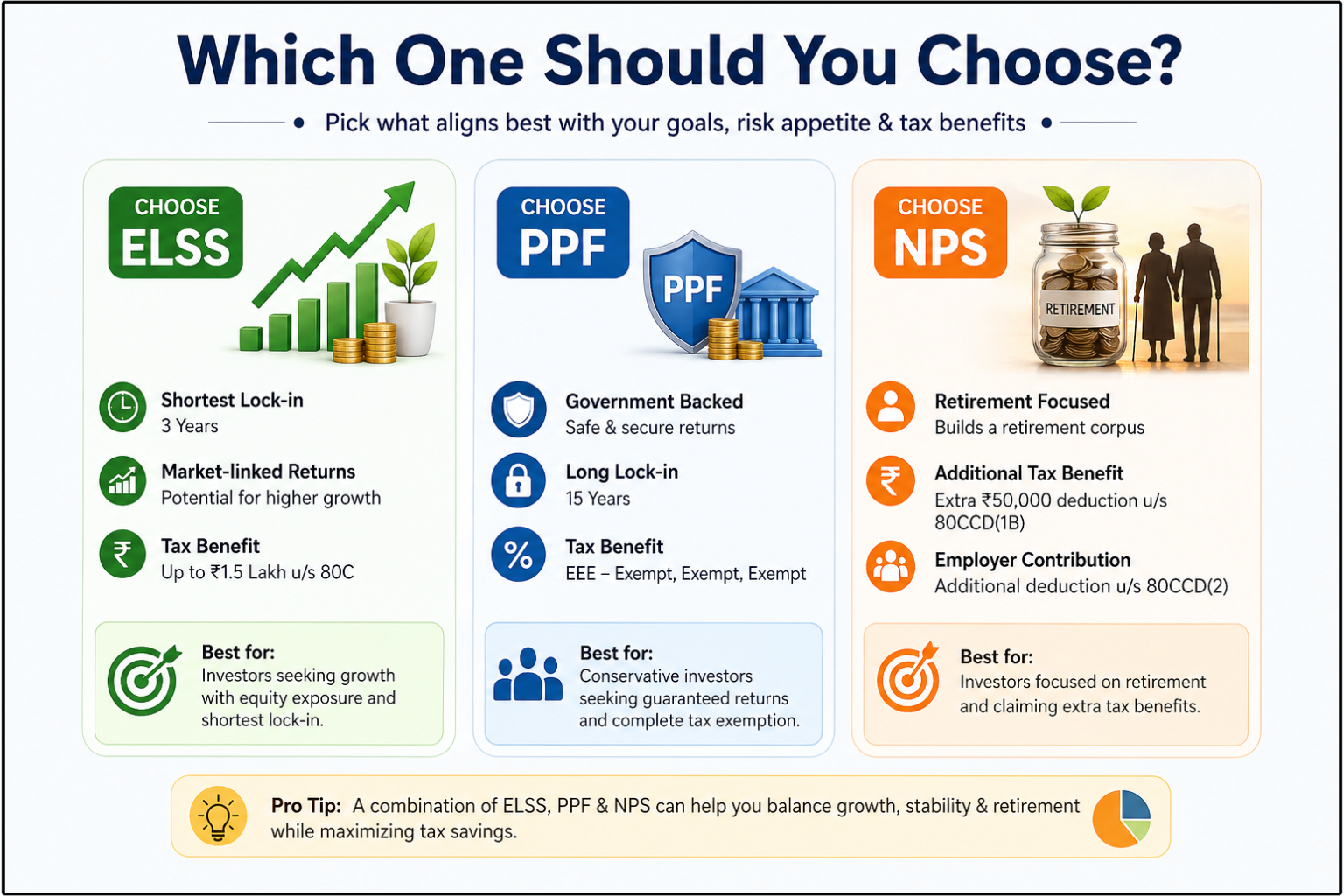

Which One Should You Choose?

Choose ELSS if you want the shortest lock-in, are comfortable with market-linked returns, and are investing for wealth creation alongside tax saving. It works well for individuals with a 5 to 10-year investment period who want equity exposure without committing to a retirement-only product.

Choose ELSS if you want the shortest lock-in, are comfortable with market-linked returns, and are investing for wealth creation alongside tax saving. It works well for individuals with a 5 to 10-year investment period who want equity exposure without committing to a retirement-only product.

Opt for PPF if you want assured, government-guaranteed returns with full tax exemption throughout the investment cycle. It suits conservative investors, first-time savers, and those in higher tax brackets who want to build a safe, long-term corpus without any exposure to market volatility. The 15-year horizon also instils financial discipline that works well for long-term goals like children’s education or a retirement buffer.

Choose NPS if retirement planning is your primary goal and you want to claim the additional ₹50,000 deduction under Section 80CCD(1B) over and above the ₹1.5 lakh Section 80C limit. It is particularly valuable for salaried professionals whose employers also contribute to NPS, as employer contributions bring an additional deduction under Section 80CCD(2).

Many investors use a combination of all three, ELSS for growth, PPF for stability, and NPS for dedicated retirement savings and the extra tax deduction. Together, they cover the full spectrum of tax efficiency, risk appetite, and financial goals.

Conclusion

ELSS vs PPF vs NPS each address a different financial need. ELSS is built for growth, PPF for safety, and NPS for retirement income. What they share is the ability to reduce your tax liability, each in a distinct and complementary way. The right choice is rarely one instrument in isolation, it is the combination that fits your income, your goals, and how far away those goals are. Understanding the tax treatment of each is the starting point for making that decision well.

FAQs

| 1.Can I invest in ELSS, PPF, and NPS at the same time? |

| Yes. ELSS and PPF both fall under the ₹1.5 lakh Section 80C ceiling. NPS contributions under Section 80CCD(1B) offer a separate ₹50,000 deduction, making the combined maximum deduction up to ₹2 lakh per year. |

| 2.Which of these can help build a passive income stream? |

| NPS is specifically designed for this through annuity payouts post-retirement, providing regular income. ELSS and PPF primarily build a lump sum corpus rather than structured income. |

| 3.Is the PPF maturity amount taxable? |

| No. PPF enjoys EEE status, contributions, interest, and the maturity corpus are all fully exempt from tax. |

| 4.Are these investments affected by interest rate cycles or policy changes? |

| PPF returns are directly influenced by government-declared rates, which may change quarterly. ELSS and NPS are indirectly affected through market movements and economic cycles. |

| 5.How portable are these investments if I move cities or change jobs? |

| All three are highly portable. However, NPS stands out as it is designed to remain active across employers, sectors, and locations without disruption. |

| 6.What is one overlooked limitation of these instruments? |

| The one overlooked limitation of these instruments is over-allocation. Many investors lock too much money into tax-saving instruments, reducing flexibility for other opportunities or liquidity needs. |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}