A Fixed Deposit (FD) is a savings instrument offered by banks and financial institutions that allows investors to deposit money for a predetermined period in exchange for a fixed rate of interest. FDs are widely used by conservative investors because they offer predictable returns and are not directly affected by stock market volatility.

As of June 2026, FD interest rates offered by scheduled banks range from approximately 2.75% p.a. to 8.10% p.a. for regular depositors across tenures ranging from 7 days to 10 years. The highest FD interest rates in India 2026 are largely offered by small finance banks and select NBFCs, while public sector and major private sector banks continue to provide comparatively lower but more established deposit options.

Among private sector banks, institutions such as Bandhan Bank, DCB Bank, and CSB Bank currently offer some of the best FD rates in India, often exceeding the rates available at larger private sector banks.

Meanwhile, small finance banks, including Suryoday Small Finance Bank, Utkarsh Small Finance Bank, and Jana Small Finance Bank, continue to dominate the list of banks offering the highest interest rates in India for fixed deposits.

This blog provides a detailed bank-by-bank comparison of the best FD rates in India, highlights the institutions offering the highest returns, and explains the key factors investors should consider before choosing a fixed deposit in 2026.

Highest FD Interest Rates in India 2026

The table below compares selected banks offering some of the highest FD rates in India as of 16 June 2026.

| Bank | Highest FD Rate

(% p.a.) |

1-Year FD Rate

(% p.a.) |

3-Year FD Rate

(% p.a.) |

5-Year FD Rate

(% p.a.) |

| Suryoday Small Finance Bank | 8.10 | 7.25 | 7.25 | 7.90 |

| Jana Small Finance Bank | 7.77 | 7.00 | 7.50 | 7.77 |

| ESAF Small Finance Bank | 7.75 | 4.75 | 7.75 | 6.00 |

| Utkarsh Small Finance Bank | 8.10 | 6.00 | 7.50 | 7.00 |

| Ujjivan Small Finance Bank | 7.65 | 5.50 | 7.25 | 7.20 |

| Shivalik Small Finance Bank | 7.80 | 6.00 | 6.75 | 6.25 |

| Equitas Small Finance Bank | 8.00 | 6.35 | 7.10 | 7.00 |

| Bandhan Bank | 7.25 | 7.00 | 7.25 | 7.25 |

| DCB Bank | 7.50 | 6.50 | 7.50 | 7.00 |

The rates may vary based on deposit tenure, customer category, and bank-specific schemes. Therefore, you must verify the latest rates on the respective bank’s official website before investing.

Bank-by-Bank FD Interest Rate Comparison 2026

While small finance banks offer some of the highest FD interest rates in India, several public sector banks continue to attract investors seeking stability, extensive branch networks, and government ownership.

The table below compares FD rates offered by major public sector banks as of 16 June 2026:

| Bank | Highest FD Rate

(% p.a.) |

1-Year FD Rate

(% p.a.) |

3-Year FD Rate

(% p.a.) |

5-Year FD Rate

(% p.a.) |

| Indian Bank | 6.20 | 6.10 | 6.15 | 6.05 |

| Punjab & Sind Bank | 6.85 | 5.85 | 5.95 | 5.95 |

| Bank of India | 6.70 | 6.50 | 6.70 | 6.00 |

| Union Bank of India | 6.65 | 6.20 | 6.10 | 6.00 |

| Indian Overseas Bank | 6.60 | 6.50 | 6.40 | 6.10 |

| Canara Bank | 6.60 | 5.50 | 6.25 | 6.25 |

| Punjab National Bank | 6.60 | 6.25 | 6.30 | 6.35 |

| State Bank of India | 6.45 | 6.25 | 6.30 | 6.05 |

| UCO Bank | 6.60 | 6.10 | 6.00 | 6.00 |

Alongside the banks featured in the highest FD rate comparison, several private sector banks offer competitive fixed deposit returns across different tenures:

| Bank | Highest FD Rate

(% p.a.) |

1-Year FD Rate

(% p.a.) |

3-Year FD Rate

(% p.a.) |

5-Year FD Rate

(% p.a.) |

| IDFC FIRST Bank | 7.35 | 6.50 | 7.35 | 6.75 |

| CSB Bank | 7.35 | 5.00 | 5.75 | 5.75 |

| City Union Bank | 7.15 | 6.65 | 6.50 | 6.55 |

| Dhanlaxmi Bank | 7.25 | 6.25 | 7.25 | 6.50 |

| DBS Bank | 6.85 | 6.30 | 6.40 | 6.25 |

| ICICI Bank | 6.50 | 6.25 | 6.50 | 6.50 |

| IDBI Bank | 6.50 | 6.20 | 6.35 | 6.25 |

| HDFC Bank | 6.50 | 6.25 | 6.45 | 6.40 |

| Axis Bank | 6.45 | 6.25 | 6.45 | 6.45 |

Their rates may not match those offered by leading small finance banks, but investors might still prefer these institutions for their strong balance sheets, extensive digital banking services, and nationwide presence.

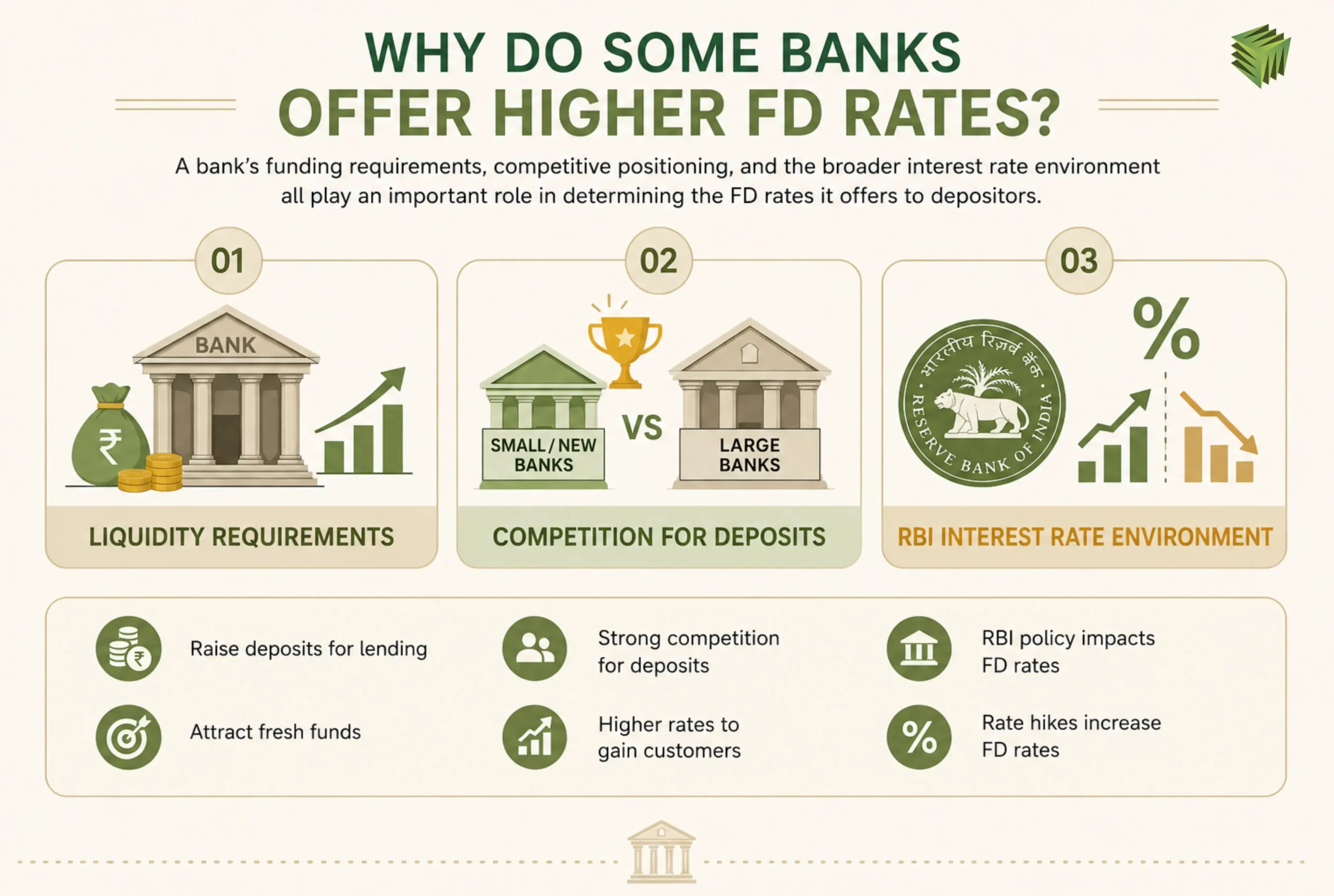

Why Do Some Banks Offer Higher FD Rates?

While the tables above highlight the banks offering the highest FD interest rates in India, the differences in returns are not random.

Liquidity Requirements

Banks rely on customer deposits to fund their lending activities. When a bank experiences strong loan demand or needs to strengthen its deposit base, it may offer higher FD rates to attract fresh funds. This is one of the primary reasons why several small finance banks offer higher fixed deposit rates than larger banking institutions.

Competition for Deposits

The banking sector is highly competitive, with institutions competing for retail deposits. Smaller banks and newer private sector banks usually offer higher interest rates to attract customers from established players such as SBI, HDFC Bank, and ICICI Bank. Offering some of the best FD rates in India helps these banks expand their customer base and grow deposits more quickly.

RBI Interest Rate Environment

The Reserve Bank of India’s monetary policy significantly influences FD rates across the banking sector. When the RBI raises policy rates, banks generally increase deposit rates to attract funds and maintain lending operations. Conversely, during periods of rate cuts, banks may reduce FD rates. As a result, changes in the RBI’s interest rate cycle have had a direct impact on the highest FD rates in India available to investors.

Risks of Chasing the Highest FD Rates

Although higher FD rates can increase returns, you should not make decisions based solely on the highest interest rates in India. You must evaluate the bank’s financial strength, deposit safety, government interference, and withdrawal flexibility when selecting a fixed deposit.

Here are some risk factors that are associated with FDs offering high rates:

- Credit and Default Risk:

Institutions offering significantly higher FD rates may be doing so because they need to attract deposits quickly or have limited access to lower-cost funding sources. In difficult cases, this can indicate a higher risk of financial stress and increase the possibility of delayed or defaulted payments.

- Limited Deposit Protection:

Bank fixed deposits are covered by the Deposit Insurance and Credit Guarantee Corporation (DICGC), which insures deposits up to ₹5 lakh per depositor per bank. However, corporate FDs and many NBFC FDs do not enjoy the same level of protection, increasing the potential risk to investors.

- Liquidity and Premature Withdrawal Restrictions:

High-interest FDs may come with stricter withdrawal conditions, lock-in periods, or higher penalties for premature closure. This can reduce flexibility if funds are required before the maturity date.

- Regulatory and Compliance Concerns:

Financial institutions offering unusually high returns may occasionally face increased regulatory scrutiny. In severe situations, regulators may impose operational restrictions or withdrawal limits, which can affect depositors’ access to funds.

Who Should Invest in High-Interest FDs?

High-interest fixed deposits are not suitable for every investor due to their elevated risk profile. They are generally better suited to individuals who understand the trade-off between higher returns and potentially higher risk.

The ideal investor profile for high-interest FDs is:

- Risk-Tolerant Investors: Investors who understand credit risk and are comfortable taking on a higher level of issuer risk in exchange for potentially higher fixed-income returns may consider high-interest FDs.

- Surplus Capital Holders: Individuals who have already built an emergency fund and secured their essential savings may allocate a small portion of their surplus capital to high-yield fixed deposits.

- Aggressive Fixed-Income Investors: Investors seeking returns that may outpace inflation and traditional bank FD rates may select high-interest FDs as part of their fixed-income allocation.

- Portfolio Diversifiers: Investors with significant holdings in traditional bank deposits may consider adding carefully selected, highly rated corporate FDs or small finance bank FDs to diversify their income-generating investments.

Final Thoughts

The search for the highest FD interest rates in India 2026 should go beyond comparing percentages on a rate sheet. While small finance banks currently offer some of the highest FD rates in India, higher returns are only one part of the investment decision.

A well-chosen fixed deposit balances return, safety, liquidity, and financial objectives. In many cases, a slightly lower interest rate from a stronger institution may be more suitable than the highest available rate.

Ultimately, the best FD rates in India are not necessarily those offering the highest return, but those that align with your risk tolerance, investment horizon, and income requirements. Before investing, compare rates across multiple institutions, diversify deposits where appropriate, and review the latest FD schedules directly from the bank’s official website.

FAQs

Which bank offers the highest FD interest rates in India in 2026?

As of June 2026, several small finance banks, including Suryoday Small Finance Bank, Utkarsh Small Finance Bank, and Equitas Small Finance Bank, offer FD rates of up to 8.00%-8.10% per annum for select tenures, making them among the highest-paying banks in India.

Are high-interest FDs safe for investors?

High-interest FDs can be safe when offered by regulated institutions, but higher returns often come with additional risks. Investors should assess the bank’s financial strength, deposit insurance coverage, credit profile, and regulatory standing before investing.

Are FD deposits fully insured in India?

No. Deposits with banks are insured by the Deposit Insurance and Credit Guarantee Corporation (DICGC) up to ₹5 lakh per depositor per bank, including both principal and accrued interest. Amounts exceeding this limit are not covered.

Why do small finance banks offer higher FD rates than large banks?

Small finance banks often offer higher interest rates to attract deposits and support lending growth. Larger banks typically have broader funding sources and stronger brand recognition, reducing their need to offer aggressive deposit rates.

Should I invest all my money in the highest-paying FD?

If you concentrate all investments in a single high-yield FD, it may increase institution-specific risk. Many investors prefer spreading deposits across multiple banks and investment products to improve diversification, liquidity, and overall portfolio stability.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}