When Palki Sharma walked out of WION, the cameras kept rolling. The set looked the same. The broadcast went out on schedule. What changed was harder to measure — the specific editorial instinct, the delivery, the point of view that had made the channel worth watching for a particular kind of viewer. Her later exit from Network18 confirmed what her WION departure had hinted at: some professionals outgrow institutional frameworks entirely.

Mutual fund investors face a structurally similar situation when the person managing their money decides to leave the Asset Management Company (AMC). The fund continues. The Net Asset Value (NAV) is calculated daily. Units remain intact. But the investment philosophy, the stock selection instinct, and the risk management approach that attracted investors in the first place changes. Whether the fund remains worth holding after that individual leaves is a question far too few investors think to ask.

The Role of a Fund Manager in a Mutual Fund

Most investors look at a mutual fund’s name, its star rating, and its returns. Few stop to ask who is actually making the decisions.

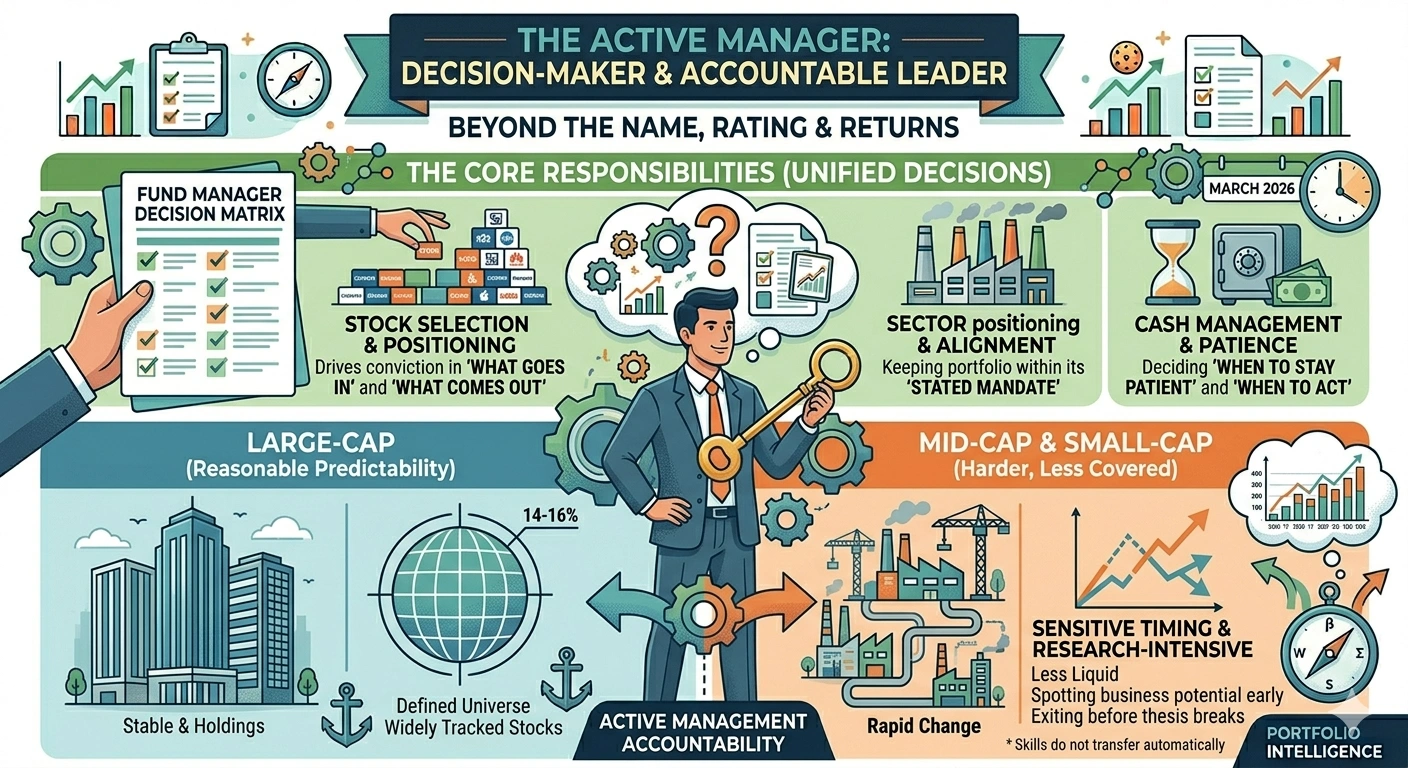

In an actively managed fund, that answer matters more than most people realise. The fund manager decides what goes in, what comes out, when to stay patient, and when to act. The research team supports that process, but the final call, and the accountability that comes with it, rests with one person.

Their responsibilities span stock selection, sector positioning, cash management, and keeping the portfolio aligned with its stated mandate. In a large-cap fund, there is reasonable predictability where the investable universe is defined and widely tracked. Mid-cap and small-cap funds are harder. Stocks are less liquid, less covered by analysts, and more sensitive to timing. The ability to spot a business before the market prices in its potential, and to exit before the thesis breaks, is a skill that does not transfer automatically when the manager changes.

Some of the popular fund managers managing mutual funds in India include:

| Fund | Category | Current Fund Manager |

| Nippon India Small Cap Fund | Small Cap | Samir Rachh |

| Parag Parikh Flexi Cap Fund | Flexi Cap | Rajeev Thakkar, Raj Mehta, Raunak Onkar |

| HDFC Flexi Cap Fund | Flexi Cap | Amit Ganatra, Dhruv Mucchal |

| ICICI Prudential Bluechip Fund | Large Cap | Anish Tawakley |

| Motilal Oswal Midcap Fund | Mid Cap | Rakesh Shetty, Swapnil Mayekar, Ankit Agarwal |

| SBI Small Cap Fund | Small Cap | R. Srinivasan |

Why Do Fund Managers Leave?

Fund manager exits happen more often than investors tend to assume. The triggers differ, but certain patterns surface repeatedly:

- Professional ambition: Working within a large institution means accepting constraints — fixed mandates, risk guardrails, and quarterly performance scrutiny. Over time, some managers find these boundaries incompatible with how they want to think about investing. Leaving to build an independent firm gives them the freedom to back their own convictions without answering to anyone else.

- AUM pressure: A growing fund is, paradoxically, a harder fund to manage well. Taking a meaningful position in a promising mid-cap company is feasible at ₹500 crore. At ₹50,000 crore, the same move shifts the price before the buying is done. Managers who built their reputation on early-stage stock identification eventually find that scale works against them.

- Compensation: The PMS industry in India has expanded considerably, and performance-linked structures available there are simply not replicable in a salaried AMC setup. For a manager with a strong track record, the financial case for staying at a fund house weakens over time.

- Internal restructuring: Mergers, ownership changes, or shifts in senior leadership can quietly alter the culture of a fund house. Departures that follow such events are rarely about a better offer elsewhere — they reflect a change in environment that no longer suits the individual.

- Personal reasons: Some exits have nothing to do with the market or the industry. Health, family, exhaustion, or a considered decision that a long career has run its natural course — these departures draw less attention but carry equal weight for investors in the affected funds.

What Is the Impact of a Fund Manager Leaving?

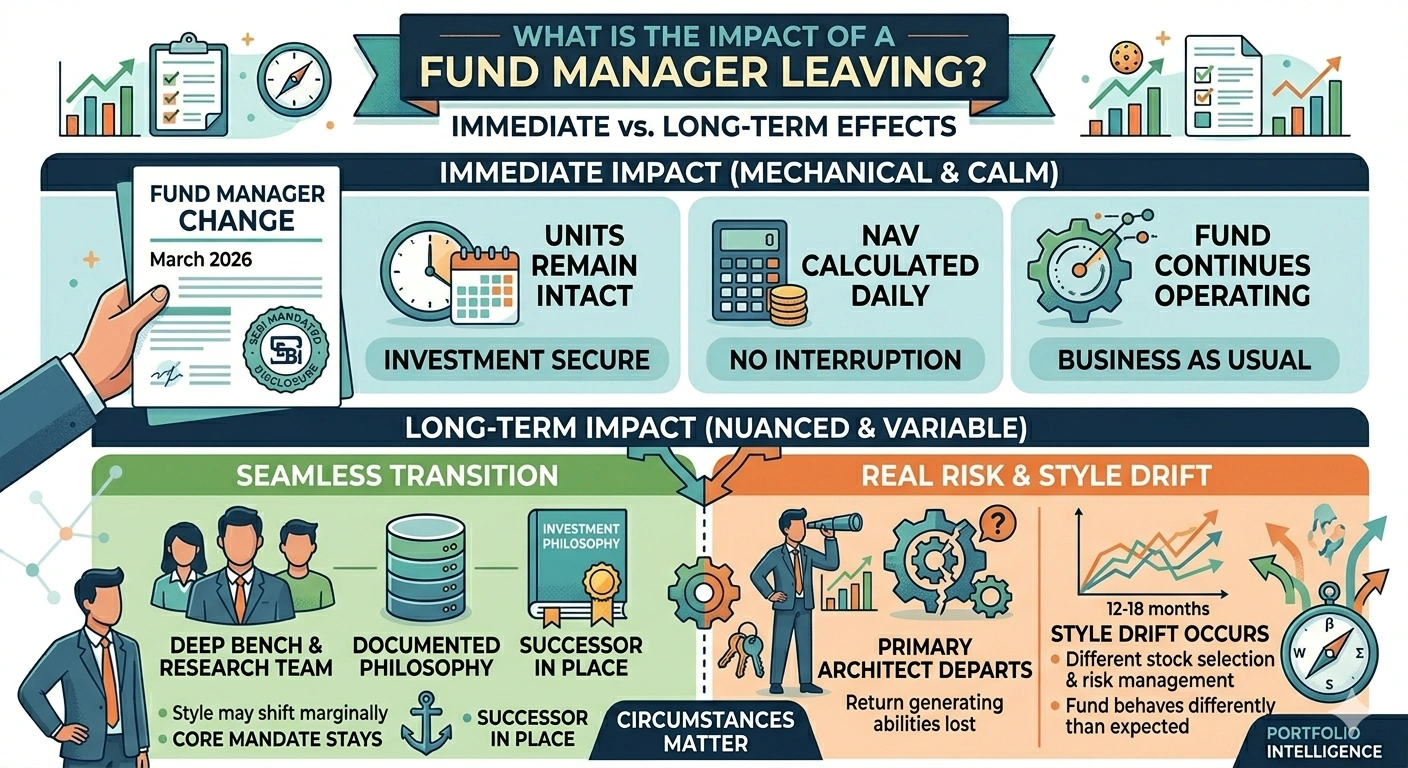

The immediate impact is largely mechanical and calm. SEBI mandates that AMCs disclose fund manager changes to investors within a defined timeframe. Your units remain intact. The NAV continues to be calculated daily. The fund does not stop operating.

The longer-term impact, however, is more nuanced and depends heavily on the circumstances. In cases where the AMC has a deep bench including a well-developed research team, a clearly documented investment philosophy, and a successor who has been part of the existing process; the transition is often seamless. The portfolio may shift marginally in style, but the core mandate stays intact.

Where the risk is real is when the departing manager was the primary architect of the fund’s return generating abilities. The subtler risk is what practitioners call style drift — where the new manager, while maintaining the same fund name and mandate on paper, approaches stock selection and risk management differently. Investors who chose the fund for a particular style may find, over 12–18 months, that the fund no longer behaves as expected.

Recent Case Studies of Fund Managers Leaving in India

Roshi Jain- HDFC (2025)

Roshi Jain resigned from HDFC AMC in November 2025 after a four-year stint, having managed over ₹1.33 lakh crore across three flagship schemes — HDFC Flexi Cap Fund, HDFC Focused Fund, and HDFC ELSS Tax Saver Fund. She had taken charge of these funds in July 2022, immediately following Prashant Jain’s exit, and delivered consistent outperformance.

HDFC AMC appointed Chirag Setalvad to manage the Flexi Cap Fund from December 8, 2025 — an internal succession from a long-tenured equity manager. For investors, the transition represented HDFC’s second major fund manager change in three years on its largest equity scheme: a meaningful signal to monitor, even if the institutional process remained intact.

Pankaj Tibrewal- Kotak AMC (2023)

Pankaj Tibrewal spent nearly 14 years at Kotak Mahindra AMC, growing Kotak Emerging Equity Fund from ₹113 crore to ₹36,000 crore — making it India’s second-largest mid-cap fund — and Kotak Small Cap Fund from ₹127 crore to ₹13,000 crore.

He resigned in late 2023 to pursue an entrepreneurial journey, and Kotak AMC appointed Harish Bihani from ICICI Prudential as his replacement. His departure was significant because his stock selection style — focused on emerging businesses in early growth cycles — was deeply personal and not easily replicable by a successor.

He went on to found IKIGAI Asset Manager, a boutique investment firm focused on long-term compounding. Investors who had chosen Kotak Small Cap and Emerging Equity specifically for Tibrewal’s approach were advised to observe the new manager’s portfolio construction before committing fresh capital.

What Are Some Things You Can Do When a Fund Manager Leaves?

The instinct to redeem the moment a fund manager exit is announced is almost always counterproductive. However, here are a few things that investors can do upon learning of the exit:

- Do not redeem immediately: Exit loads and capital gains tax apply. Thus, acting on announcement day is rarely the right move.

- Give it two to three quarters: Observe how the new manager constructs and adjusts the portfolio before drawing conclusions. It may be the case that the new approach aligns with your goals, and it would be sensible to continue with the fund.

- Check the succession quality: An internal appointment with an established track record is meaningfully different from an emergency external hire.

- Watch for style drift: Review quarterly portfolio disclosures on AMFI. Any shifts in sector allocation or market cap positioning are early warning signs.

- If uncertain, consider index funds: They carry zero manager dependency by design.

Conclusion

A fund manager’s departure is not, by itself, a reason to exit. It is a reason to pay closer attention — to the AMC’s response, the quality of the successor, and the fund’s behaviour over the following quarters. The investor who monitors systematically and acts on evidence will consistently outperform the one who either panics immediately or ignores the change entirely. Know who manages your money. Understand what changes when they leave. That awareness alone places you ahead of the majority of retail investors in this market.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}