Summary

- An emergency fund is a reserve that protects investors during a financial crisis.

- Monthly living expenses and coverage period for financial security are required to calculate an adequate amount of the emergency fund.

What is an Emergency Fund?

An emergency fund is a cash reserve set aside to cover unforeseen and unplanned expenses or financial emergencies. It helps to support any unexpected expenses.

Emergency funds are used for sudden expenses that are not a part of routine expenses. Providing readily accessible funds during emergencies helps investors manage unforeseen expenses without affecting their broader financial strategy. It can be used for sudden medical expenses, unplanned business disruptions, sudden job loss, etc.

How does an Emergency Fund work?

An emergency fund is a reserve of readily accessible money that helps investors manage unexpected expenses while keeping their broader financial plan on track.

In the event of a financial emergency, an emergency fund acts as a financial cushion, helping investors manage unexpected expenses without affecting their long-term financial goals. It reduces the chances of panic and chaos during an emergency. After the funds are withdrawn, it is important to restore or replenish the fund to continue the financial support for future occurrences.

- The Safety Net concept: This provides financial safety by maintaining separate funds for unknown expenses, such as sudden job loss, medical expenses, major repairs, and bills.

- The Ideal Amount: This is the amount that investors preserve, i.e., 3-to-6 months’ worth of essential living expenses from their earnings to support unforeseen uncertainties.

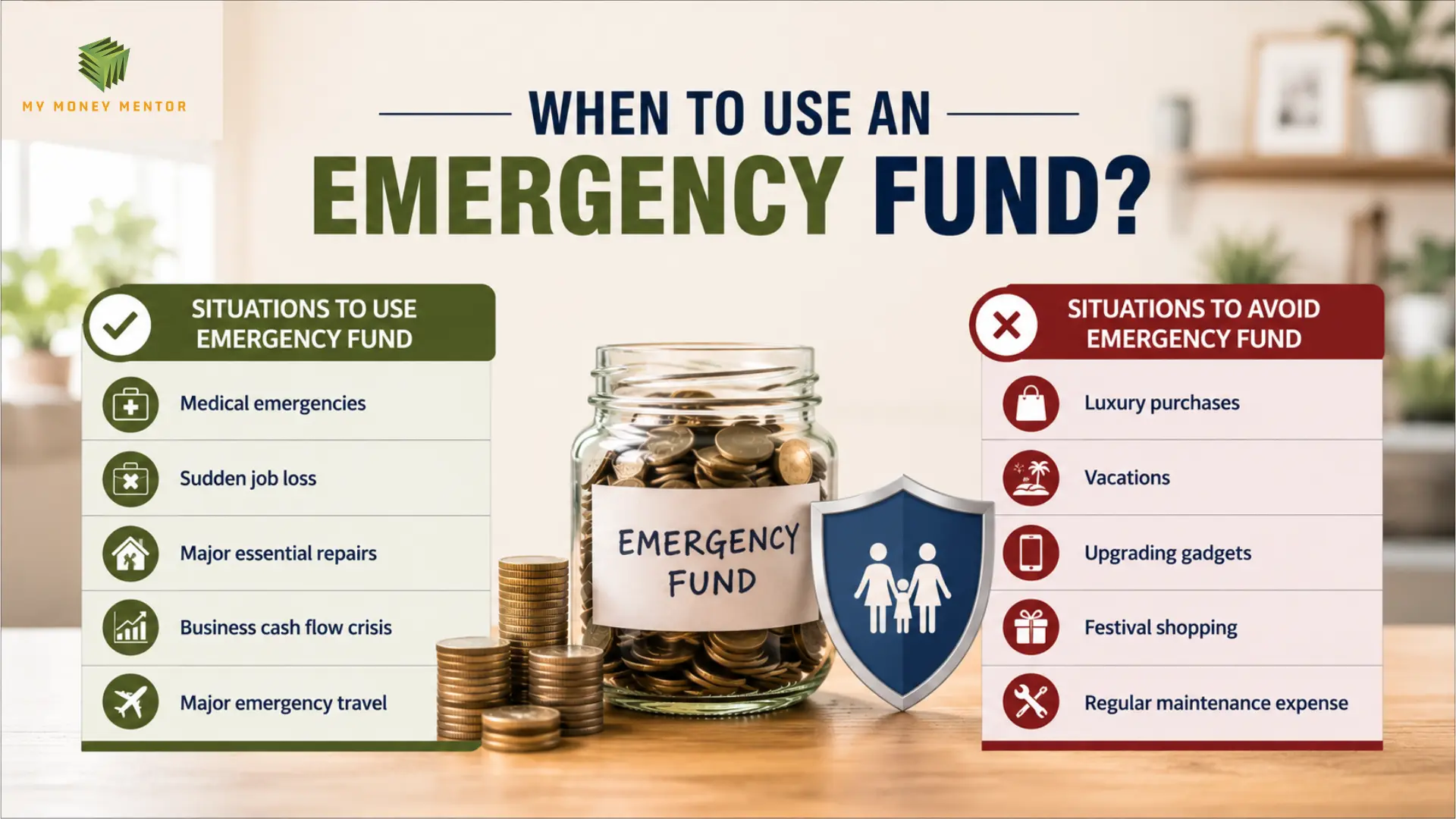

When to use an Emergency Fund?

The most important factor in an emergency fund is identifying which types of expenses qualify. Therefore, any major expense that is urgent, unexpected, and unavoidably necessary requires support from emergency funds.

The following table shows a few situations on when to use and when not to use an emergency fund.

| Situations to use emergency fund | Situations to avoid emergency fund |

| Medical emergencies | Luxury purchases |

| Sudden job loss | Vacations |

| Major essential repairs | Upgrading gadgets |

| Business cash flow crisis | Festival shopping |

| Major emergency travel | Regular maintenance expense |

Where to keep an Emergency fund?

Emergency funds can be secured through various means, depending on their accessibility.

- Savings account: Maintaining a separate bank savings account solely for emergencies. It helps to provide immediate accessibility and urgent support available through cash and online transactions. It has high liquidity and low risk because the bank maintains the funds.

- Sweep-in fixed deposit: This is an FD that is directly linked to the savings account. It provides liquidity similar to a savings account and earns better interest. Since it is linked to the savings account, any excess or deficit is balanced by sweeping funds between them.

- Liquid or Overnight Funds: These are relatively low-risk mutual funds that invest in short-term money market instruments. It provides better returns than a savings account and can be redeemed during emergencies.

- Overdraft against FDs: Investors who maintain fixed deposits can access overdrafts on FDs. It allows investors to borrow a certain amount, limited to the value of their fixed deposit. They are required to pay interest on the exact amount that they borrowed. It allows borrowing money without breaking the FD while the remaining FD continues to generate interest.

Investors may allocate their funds into portions and invest each portion in different sources to maintain a balance.

How Much Emergency Fund is Enough?

The amount of emergency funds cannot be fixed due to the different lifestyles of people in India. However, an adequate emergency fund is determined by the investor’s job security, income stability, and the responsibilities of family members.

Financial experts in India generally recommend maintaining an emergency fund equivalent to three to 3 to 6 months’ essential expenses. As a general guideline, single investors without financial dependents can target an emergency fund equivalent to 3 months’ essential expenses. Investors with financial responsibilities toward family members or dependents should ideally maintain an emergency fund sufficient to cover 6 months of essential expenses.

Since entrepreneurs, freelancers, and business owners may experience income fluctuations, they should consider building an emergency fund sufficient to meet 9 to 12 months of essential household expenses. This will allow them to have better financial security.

Calculation of an Emergency Fund (Real-World Example)

There are a few steps to calculate the amount of an emergency fund. They are mentioned below.

Step 1: Calculate your monthly expenses: List your unavoidable expenses that need to be paid every month without fail.

Step 2: Choose your coverage period: Select an appropriate coverage period that aligns with your financial situation and the level of security you wish to maintain.

Step 3: Multiply your expense by the coverage period: Multiply the amount of your monthly expenses by the coverage period you selected. The total will be the amount of emergency fund you should maintain depending on your financial situation.

Let’s understand with the help of an example.

An investor, Mr S, is a small business owner who earns seasonal income. Since his income is not stable, he wants to maintain an emergency fund for urgent expenses.

The monthly expense of Mr S is ₹30,000, which includes his rent, electricity bill, food and utilities, etc., and he decided to maintain it for a period of 6 months. Therefore, the total amount that he requires to maintain in an emergency fund was ₹1,80,000.

Why is an Emergency Fund important for Indian households?

Maintenance of emergency funds is very important for Indian households for various reasons. Some of them are mentioned below.

- Manage over-expensive medical expenses: Even with proper health insurance, Indian households often face out-of-pocket costs, including non-medical expenses, consumables, visits and travels, non-network hospital charges, etc. An emergency fund immediately supports these expenses without having to take a loan.

- Income security: Due to economic volatility and sudden layoffs by companies, the income status may be disrupted. Maintaining an emergency fund provides people with enough finances while they search for a suitable job opportunity.

- Preserve long-term goals: Investors often redeem their funds or investments during a crisis, which disrupts their overall financial goals. An emergency fund provides them with support for their expenses without compromising their long-term wealth-creation process.

- Unplanned family obligations: In Indian culture, family is very important. Financial responsibilities and emergencies often extend to support extended family members as well. Therefore, an emergency fund can provide financial assistance to extended family members without straining their immediate family.

How to build an Emergency Fund?

The steps to build an emergency fund are mentioned below.

Step 1: Calculate the baseline target: Determine the cost of your unavoidable living expenses, including rent, utility bills, EMIs, etc. Avoid including vacation and luxury expenses. Multiply the total living expense by the coverage period for how long you want financial security. This will give you the baseline target for investing.

Step 2: Choose the Right place to invest: Choose the option that will provide safety and immediate liquidity to your funds. Instead of investing in stocks where you might experience loss during redemption, choose a high-yielding savings account, sweep-in FD, or a low-risk mutual fund.

Step 3: Automate your contribution: Set up a direct transfer from your normal savings account to your emergency fund immediately after you are paid and treat it like a recurring monthly deposit.

Step 4: Start small and scale up: You do not have to begin with a huge emergency fund. Instead, you can increase your fund slowly and gradually increase your contributions when your income supports it.

Step 5: Protect the fund: Withdraw or redeem the funds only when they are urgently required. Keep these funds separated and avoid using them for covering regular expenses. If the funds are withdrawn, prioritise replenishment or restoration of the funds immediately for further financial security.

Benefits of an Emergency Fund

The benefits of an emergency fund are mentioned below.

- Prevents high-interest debt: Having adequate cash in hand or separate savings helps investors to reduce dependence on high-interest loans during emergencies, especially when they are already facing a financial crisis.

- Protects long-term goals: A separate savings account for sudden expenses provides a cushion to support the investments made for long-term financial goals and eliminates the chance of redemption during emergencies.

- Reduces financial stress: An emergency fund allows investors to maintain financial security by providing immediate access to funds when needed. Therefore, they help investors to reduce their overall financial stress.

- Greater financial flexibility: An emergency fund helps investors to maintain flexibility while going through sudden occurrences of unemployment, medical expenses, etc. This provides them the room to make the right decision rather than making desperate decisions during a crisis.

Common Mistakes while using the Emergency Fund

The common mistakes made while using an emergency fund are mentioned below.

- Using funds for non-emergencies: Withdrawing or redeeming the emergency funds for spending on expenses that may feel urgent but are not very important. Avoid redeeming emergency funds for vacations, new gadgets, etc.

- Confusing predictable expenses with emergencies: Emergency funds are for unforeseen and sudden expenses. Investors often assume predictable future expenses as emergencies and spend on expenses such as car and house repairs.

- Keeping money in normal accounts: Not having a separate account for emergency funds and keeping it with the normal savings account may lead it to being spent on daily expenses.

- Failing to replenish the fund: Many investors often forget to replenish their fund after withdrawal. This removes the financial safety net for the future possibility of a financial crisis.

- Investing in volatile assets: To generate more income using the funds, investors may invest in highly volatile stocks that may crash or decline exactly when the funds are urgently required.

Final Thoughts

An emergency fund is a separate fund that investors preserve to mitigate the sudden occurrence of financial emergencies. It creates a safety net to protect against the uncertainties.

The ideal amount for emergency funds depends on the income status, family size, and financial obligations of an investor. As per the financial experts, holding for a period of 3 to 6 months is enough for a stable income investor. However, someone who does not have a stable income may maintain the funds for 6 to 12 months. It helps to provide assistance during medical expenses, major family obligations, and to protect long-term goals, etc. After a crisis, replenish the funds to continue the financial protection rather than waiting for another crisis.

FAQs

Is a 3-month emergency fund enough for an Indian family?

A 3-month emergency fund may be sufficient for households with stable income, multiple earning members, and low financial obligations. However, families with dependents, variable income, or higher financial responsibilities may consider maintaining six months or more of essential expenses.

Should I keep my emergency fund in a savings account or a mutual fund?

A combination approach is often suitable. Keeping a portion in a savings account ensures immediate access, while the remaining amount can be parked in liquid mutual funds or sweep-in fixed deposits to potentially earn higher returns while maintaining liquidity.

How often should I review my emergency fund?

It is advisable to review your emergency fund at least once every year or whenever there is a major change in income, expenses, family size, employment status, or financial commitments.

Can I use my emergency fund for planned expenses?

No. Planned expenses such as vacations, weddings, gadgets, or home renovations should ideally be funded through separate savings. Emergency funds should be reserved only for unexpected and urgent financial situations.

What is the difference between an emergency fund and a contingency fund?

An emergency fund is typically designed to cover major unexpected events such as job loss, medical emergencies, or sudden income disruptions. A contingency fund, on the other hand, is often maintained for foreseeable but uncertain expenses such as minor repairs, travel requirements, or temporary budget overruns. Both serve different purposes but contribute to overall financial preparedness.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}