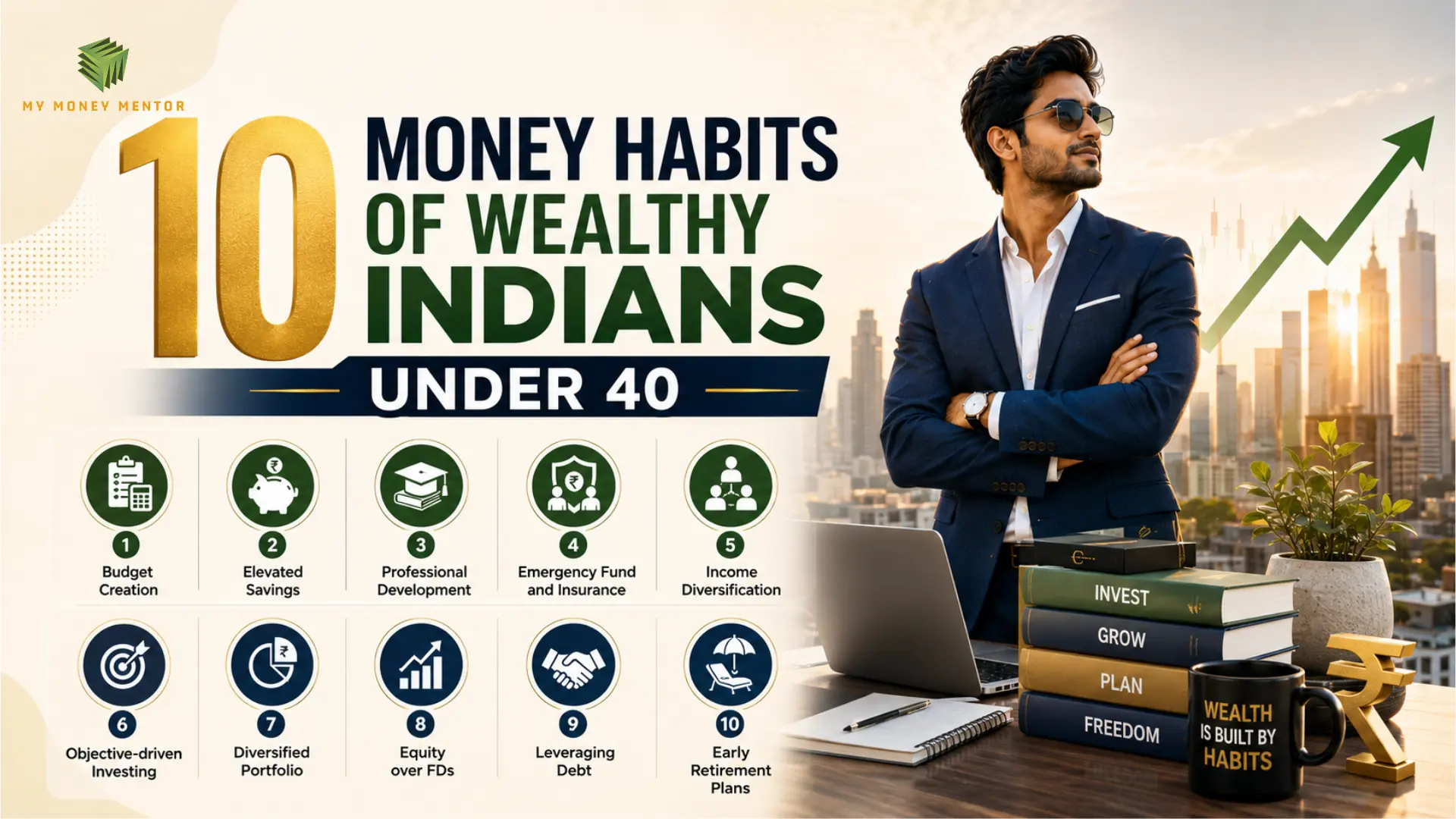

Summary

- Most wealthy citizens of India follow certain habits to earn adequate returns and continue creating long-term wealth even during a crisis.

- These habits include creating budgets, maintaining separate emergency reserves, diversifying their income sources, and investing in multiple securities to avoid unfavourable financial situations without disrupting the overall financial plan.

Building wealth before the age of 40 is rarely the result of a high income alone. Instead, it is often driven by consistent financial habits, disciplined investing, and smart money management. Wealthy Indians focus on saving regularly, investing with clear goals, diversifying their income and portfolio, and planning for long-term financial security rather than seeking quick gains.

In this article, we explore 10 money habits of wealthy Indians under 40 that contribute to sustainable wealth creation. Whether you’re just beginning your financial journey or looking to improve your money management skills, these practical habits can help you make informed financial decisions and work towards long-term financial independence.

1. Budget Creation

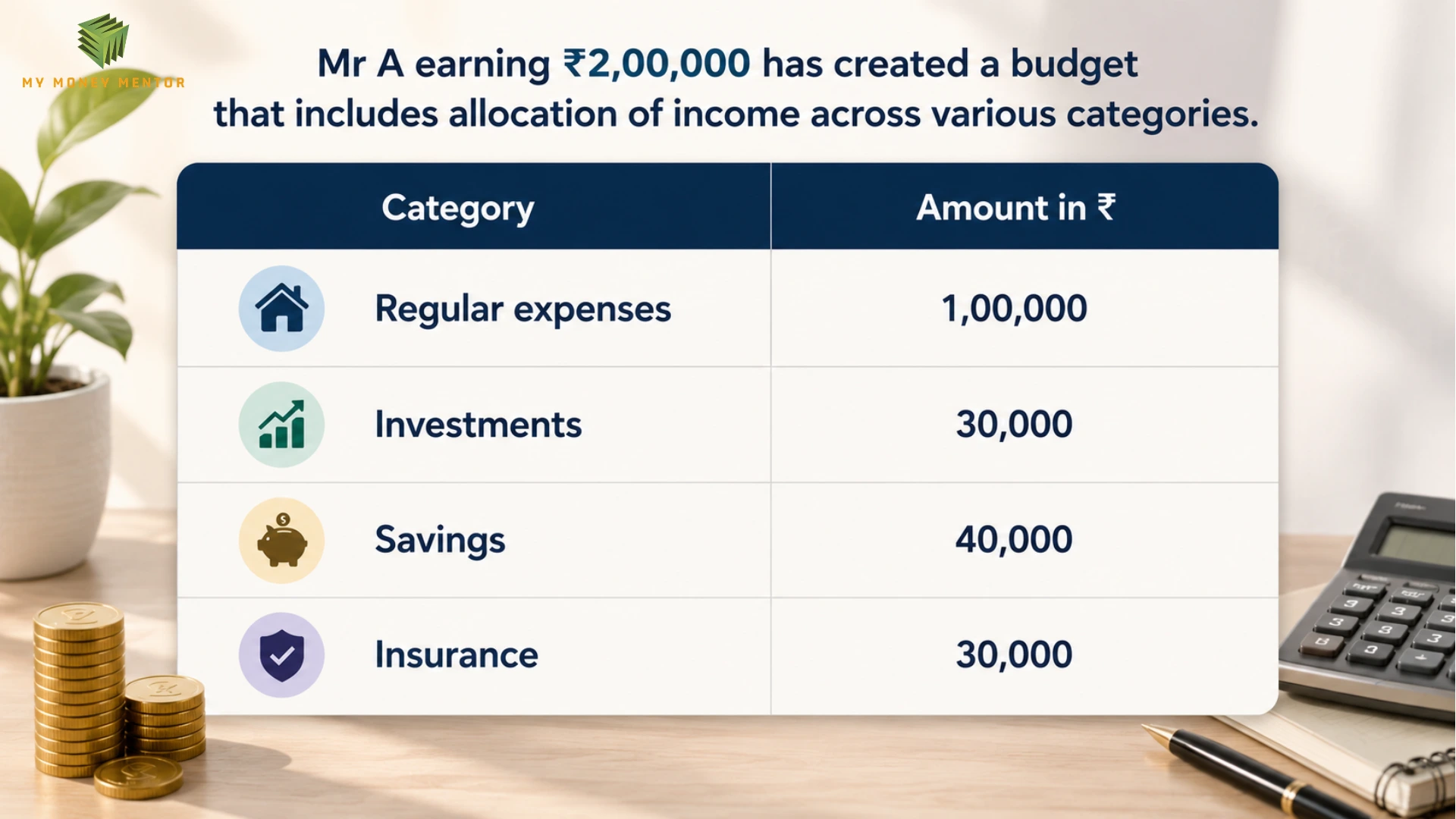

One of the most important habits that wealthy Indians follow is creating and maintaining a budget. Maintaining a budget is not only for individuals with lower incomes, but also for high-income earners who use budgets as a tool to track their expenses and savings. This helps them maintain their cash flow efficiently to achieve their financial goals.

A budget helps individuals understand their spending and helps avoid any unnecessary expenses. Most individuals are advised to save at least 20% of their income, depending on their life. This helps them allocate their funds efficiently across categories such as savings, insurance, investments, and emergency funds.

Example: Mr A, earning ₹2,00,000 a month, has created a budget that includes allocation of income across various categories.

2. Elevated Savings

Reserving a portion of income before expenses is another important habit that wealthy individuals prioritise. Instead of saving after spending on various expenses, wealthy individuals set aside a fraction of the income for savings before contributing to expenses. They automate their savings by immediately transferring the money right after receiving their salary.

Creating a savings or reserve helps them during urgent monetary requirements. Rather than selecting debt or loans in an emergency, individuals can use the money set aside as savings. The main intention is not only to save money but also to generate future returns.

Example: A person, Mr S, earning ₹2,00,000 a month used to save a fraction of his income after spending on expenses, i.e., ₹10,000. At the end of the year, he could only save ₹1,20,000. That way he was not able to save enough.

Later, he decided to save ₹25,000 before spending, and as a result, the consistent saving before expenses increased his savings to ₹3,00,000.

3. Professional Development

Wealthy individuals work on increasing their potential to earn high income by upgrading their skills. They focus on expanding their network by participating in various training and skill-developing courses, such as artificial intelligence, technical analysis, or digital marketing.

This helps them create opportunities for future promotions and increments and to expand their knowledge, allowing them to build valuable professional relationships with colleagues, mentors, industry experts, and business leaders, creating opportunities for long-term career and financial growth. Rather than treating learning expenses as a cost, wealthy individuals consider them an investment that can improve earning potential and accelerate wealth creation.

Example: Mr D has been earning ₹2,00,000 a month working as an engineer for the last 2 years. He decided to learn a special skill that will expand his knowledge and help him in his promotion to earn more. He chose to learn Artificial Intelligence in 6 months, for which he paid a ₹10,000 monthly fee. After 6 months, he completed his course and landed a promotion. Therefore, the ₹60,000 he paid for the course was an investment for him to increase his salary.

4. Emergency Fund and Insurance

Keeping an extra portion of money, reserved only for emergencies, is practised by individuals who seek balance in their financial goals. These emergency reserves are kept separate from ordinary savings to provide financial protection during unforeseen emergencies, such as sudden medical expenses, job loss, or family emergencies.

These funds enable individuals to handle urgent expenses while keeping their investment strategy and financial objectives on track. These funds are generally invested in highly liquid options, such as savings accounts and liquid funds, to provide easy access during unforeseen financial situations.

Wealthy individuals understand the impact of a sudden financial crisis on long-term financial plans. Therefore, they prepare themselves by maintaining insurance policies that act as protection against unforeseen situations. The most commonly available insurance policies include term insurance, health insurance, fire insurance, and theft insurance.

Example: Mr B, who earns ₹20,000 monthly, has been taking a portion out of his salary and maintaining an emergency fund of ₹1,200 for 3 months to protect from possible unforeseen situations.

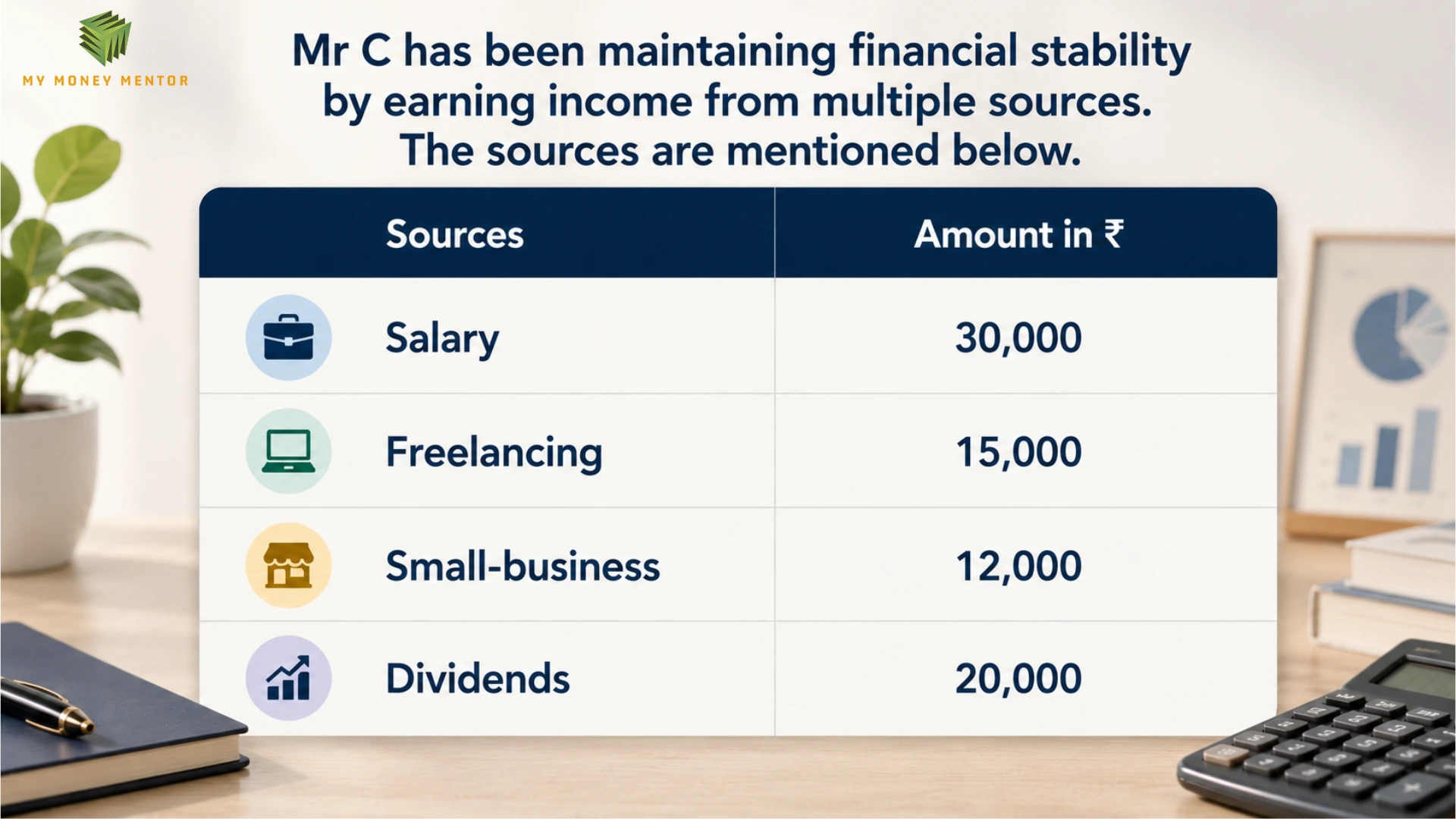

5. Income Diversification

Concentrating entirely on a single source of income limits income generation. Wealthy individuals prefer to generate income through several sources. This helps to enhance their financial stability and reduces the dependence on a single source.

Rather than relying on a single source of income, wealthy individuals typically diversify their earnings through salaries, rental income, business profits, freelancing, and other income-generating activities. This provides financial stability against financial imbalance and also promotes long-term wealth creation.

Example: Mr C has been maintaining financial stability by earning income from multiple sources. The sources are mentioned below.

6. Objective-driven Investing

Successful individuals prefer to invest in financial securities that satisfy their financial requirements. They do not prefer investing without having a proper goal or purpose. The objectives of investment can range from short-term financial needs to long-term wealth creation, such as travelling abroad, buying a house, retirement plans, and expanding a small-scale business.

While making investments, individuals should evaluate the investment objectives, risk profiles, and lock-in periods alongside their own investment goals and risk tolerance. This provides them with a clear route to wealth creation by reducing emotional decisions and staying patient during market corrections.

Example: Miss B has been investing in investment securities to satisfy her financial goals. The following table includes her goals.

| Securities | Amount in ₹ |

| House property | 30,000 |

| Retirement | 10,000 |

| Vacation abroad | 10,000 |

7. Diversified Portfolio

Wealthy individuals do not prefer to be limited to a single financial security market. They select multiple financial securities and allocate their investments accordingly to gain exposure to a wide range of markets, reducing heavy dependence on a specific market. Investments can be allocated in various securities, including stocks, bonds, government securities, mutual funds, and ETFs.

Under certain market conditions, different markets may react differently. Diversification minimises portfolio risk by spreading investments across different asset classes, ensuring that poor performance in one investment does not significantly impact overall returns. This helps successful individuals to balance the risk associated with investments and ensure effective wealth creation.

Example: Mr H has been maintaining a diversified portfolio including multiple securities to reduce the concentration risk.

| Asset Allocation | Amount in ₹ |

| Equity | 20,000 |

| Bonds | 12,000 |

| Government Securities | 15,000 |

8. Equity over FDs

Although fixed deposits offer stable and predictable returns over a specified tenure, their post-tax returns may not always be sufficient to outpace inflation and generate substantial long-term wealth. However, equity stocks can earn a higher return under favourable market conditions. Wealthy individuals do not completely abandon fixed deposits; instead, they allocate their investments strategically to meet emergency needs and short-term financial goals while maintaining liquidity and financial stability.

Investing in fixed deposits is quite popular among Indian citizens, but wealthy Indians who understand the impact of inflation and tax often diversify into equities. This provides opportunities to earn more than expected during market elevations and to secure ownership in growth-potential businesses.

Example: Miss K has prioritised her allocations on equities over FDs. She has allocated 70% of her investments in equity and 30% in FDs to earn a higher return. The objective of the allocation is to take advantage of the moving market conditions.

9. Leveraging Debt

Debt is not necessarily a bad financial decision when used responsibly and for productive purposes. The efficiency of borrowed finances depends on their utilisation. Wealthy individuals use debt or loans to invest in assets with the potential to generate returns. When borrowed funds are invested wisely, the income or returns they generate can help meet loan repayments while maintaining financial stability.

However, inefficient use of borrowed funds, including buying unaffordable luxury items or making unnecessary purchases, may result in a crisis situation during repayment obligations. Successful individuals understand the advantages and disadvantages of borrowed funds, which helps them make decisions by adding value to their financial planning.

Example: Mr R has borrowed finances for the purpose of expansion of his business and purchased machinery to increase its production. As a result, the borrowed funds were allocated wisely and generated income, which also contributed to their repayment.

10. Early Retirement Plans

Starting an early retirement plan is one of the important investments that wealthy individuals make. Instead of planning for retirement when they are close to a certain age, they prefer planning way before they reach that period, during their earning years. This helps them acquire an adequate amount of wealth through the power of compounding, providing them with the advantage of flexibility and financial independence.

Wealthy individuals understand the impact of potential economic evolution on the monetary aspects of the citizens of India. Therefore, they strategically evaluate and analyse the various options available in the market, which will facilitate them to live a financially independent life.

Example: Mr S and Mr C have started their retirement plans from the age of 25 and 29 respectively. Since Mr S started to save from a relatively young age, he could collect more returns than Mr C, because of the power of compounding.

Common mistakes that wealthy Indians avoid

There are various situations that a financially successful individual avoids to ensure long-term financial goals.

- Emotional decision: Making decisions entirely influenced by emotions is the most common mistake made by ordinary people. A successful person understands the importance of consistent investing. They make necessary decisions regarding an investment depending on its performance rather than letting their fear and greed make the decision. Holding back and not making any movement on an investment, assuming it will grow in future, may hamper the investor, in contrast.

- Lack of financial objectives: Not having a proper financial objective will result in not being able to make the correct decision. It is very important to have a goal, so that it can guide the decisions to achieve it. All wealthy individuals have certain goals that they aspire to achieve by aligning their decisions accordingly. A proper goal facilitates seamless decision-making and staying focused during unforeseen situations.

- Unreasonable debt: Borrowing debt for investing in assets that do not provide a financial advantage to the borrower may result in difficulties in the obligation of repayment. Wealthy individuals avoid borrowing loans that do not enable them to enhance their wealth creation. They use borrowed funds only for investing in assets that have the potential to create more wealth in future and add value to their financial goal.

- Concentrated investment: Wealthy individuals prefer to spread their investment across multiple securities instead of concentrating solely on a single market. This helps them minimise the concentrated impact on investments during market corrections. They diversify their investments across different markets because changes in market or economic conditions impact all securities markets.

- Unnecessary expenses: Trying to adapt a high-quality lifestyle immediately after a slight increase in revenue is not a preferable decision. Wealthy people avoid elevating their lifestyle right after an increment; instead, they increase the amount of savings. They avoid spending on unnecessary items that will not add value to their long-term wealth creation.

Conclusion

The people who gain wealth before they reach 40 have certain habits that they follow to ensure disciplined wealth creation in the long run. They prepare a budget and track their spending based on that budget. They separate a portion from their salaried income and invest in various other sources, such as emergency funds, insurance policies, early retirement schemes, and other sources that help them create additional income. They always make investments with some objective and diversify the investments across multiple securities to minimise concentration risk.

Moreover, they also avoid certain practices, such as making emotional decisions, investing without purpose, and encouraging unnecessary spending, to ensure efficient long-term wealth creation while maintaining a secure financial plan.

FAQs

How much should young professionals save every month?

There is no fixed percentage that applies to everyone. However, many financial planners recommend saving at least 20% of monthly income. Individuals can maintain a savings account depending on their lifestyle and obligations.

Why do wealthy people prefer equity investments?

Equity investments have historically provided higher long-term returns than many traditional fixed-income instruments. They also offer the potential to outperform inflation and create substantial wealth through compounding over extended periods.

What role does financial planning play in wealth creation?

Financial planning provides a structured roadmap for achieving financial goals. It helps individuals allocate resources efficiently, manage risks, monitor progress, and make informed investment decisions aligned with their objectives.

Why do wealthy individuals focus on multiple income streams?

Multiple income streams improve financial stability and reduce dependence on a single source of earnings. They also create additional opportunities for wealth accumulation and provide protection during economic or career-related disruptions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}