When deciding between taking a home loan and renting, neither option is inherently better as the right answer depends on your personal circumstances. A home loan makes more sense for someone with a stable income planning to stay in one city for several years. Renting works better for those who are early in their career or whose plans are still taking shape. The Reserve Bank of India (RBI) held its repo rate at 5.25% through the June 2026 review, which has nudged home loan rates down to some of their most comfortable levels in years. Rents, meanwhile, have picked up the pace in several metro cities. So the comparison is less about picking a winner and more about matching the choice to your income, your city, and your timeline.

Home Loan in India: How It Works

A home loan lets you borrow from a bank, repay through monthly instalments, and own the property outright once the loan is fully paid off. Here is how it plays out:

- EMI structure: Each Equated Monthly Instalment (EMI) is split between principal and interest, and the amount either stays fixed or fluctuates depending on whether you chose a fixed or floating rate.

- Down payment: Banks do not fund the entire property cost. As per RBI guidelines, the Loan-to-Value (LTV) ratio is capped at 90% for loans up to ₹20 lakh, 80% for loans between ₹20 lakh and ₹75 lakh, and 75% for loans above ₹75 lakh. The remainder comes from your own pocket as the down payment.

- Additional upfront costs: Stamp duty, registration charges, and processing fees add to the total cost beyond just the down payment.

- Tenure trade off: A longer loan tenure reduces your monthly EMI but increases the total interest paid over time, while a shorter tenure does the opposite.

- Affordability rule: According to the Reserve Bank of India, banks assume that 55 to 60% of your monthly disposable income is available for loan repayment. The higher your disposable income, the larger the loan amount you may be eligible for.

Home Loan: Advantages and Limitations

A home loan comes with real financial upside for the right buyer.

- Builds long-term equity

Every paid EMI instalment reduces the outstanding principal, which slowly turns a monthly payment into an asset that belongs to the borrower once the loan ends.

- Property appreciation

Property in India has historically gained value over long holding periods, particularly in cities with strong job growth, meaning the asset can grow while the EMI itself stays unchanged.

- Removes housing pressure after retirement

A fully repaid home takes the cost of housing out of the monthly budget during retirement, a phase when income falls, and predictable expenses matter more.

- Encourages forced savings

An EMI works like an automatic saving habit, since the money goes into building equity each month rather than requiring the borrower to consciously set it aside.

That said, ownership through borrowing has its own set of demands that not everyone is prepared for.

- Locks up income for a long period

A loan tenure stretching across two or three decades reduces flexibility for other financial goals or sudden expenses that may come up along the way.

- Involves high upfront costs

Down payment, stamp duty, registration, and interiors can together demand a sum that many first-time buyers do not fully account for in advance.

- Reduces mobility

Relocating to another city for work or opportunity becomes harder once a property and a long repayment commitment are tied to one place.

- Adds ongoing ownership costs

Maintenance, property tax, and insurance are recurring expenses that fall entirely on the owner and do not exist for someone renting the same kind of home.

Renting a Home in India: How It Works

Renting means paying a monthly amount to live in someone else’s property. It usually involves a security deposit, which can run as high as ten months’ rent in cities like Bengaluru and Mumbai. This deposit sits idle for the length of the tenancy. Rent agreements typically last eleven months and are renewed at a higher rate each time, though this varies by city and landlord.

What renting gives you is the room to breathe. No structural repairs to worry about, no decades-long obligation hanging overhead, and the freedom to pack up and switch cities without first needing to find a buyer.

Renting: Advantages and Limitations

Renting offers a different kind of value, built around freedom rather than ownership.

- Keeps cash available

Without an EMI eating into the budget, that money can be redirected toward other goals such as investments, education, or simply building a larger emergency fund.

- Requires lower upfront capital

Renting needs only a security deposit and sometimes a broker’s fee, which are far less than the down payment and related costs of buying a home.

- Removes maintenance responsibility

Structural repairs and major upkeep are the landlord’s responsibility, sparing tenants both the cost and the effort that ownership demands.

- Allows easier relocation

Tenants can move for a new job or a better locality with relatively short notice, something that becomes far harder once a property is owned.

Still, renting also has its own set of drawbacks.

- Builds no ownership or assets

Rent paid each month does not return in any form. There is no equity, no appreciation, and nothing to show for the years of payments made.

- Unpredictable rent hikes

Annual increases are common and largely set by the landlord, meaning the financial burden can keep rising without a fixed ceiling.

- Limited security of tenure

Landlords can ask tenants to vacate with short notice, and customisation of the living space is usually restricted under most rental agreements.

- Demands self-discipline to build wealth

Any financial advantage from renting depends entirely on consistently investing the money saved, which many renters do not actually follow through on.

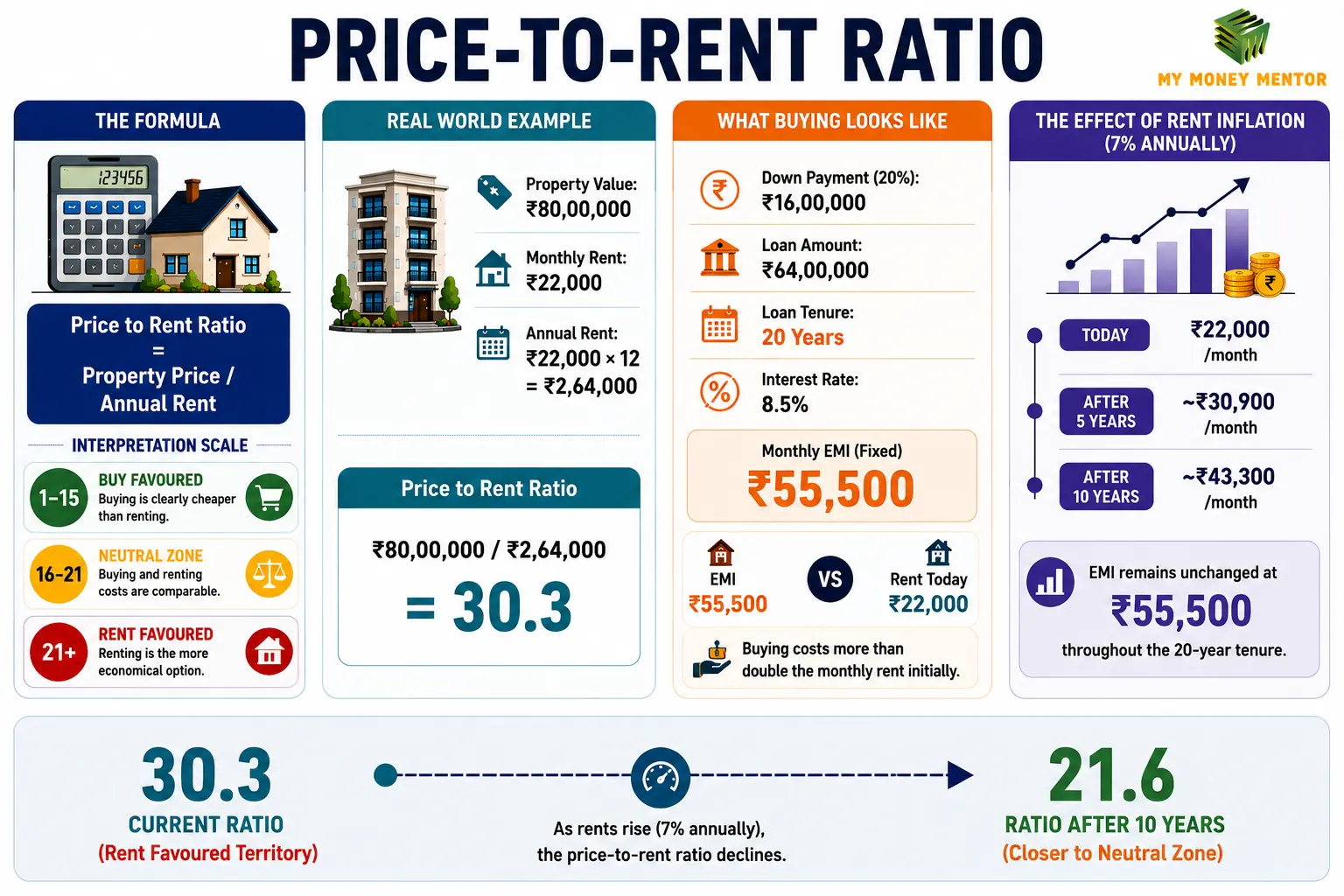

Price to Rent Ratio: A Useful Tool to Decide

The Price to Rent ratio is used to figure out whether a city’s property market favours buying or renting. It is found by taking a property’s purchase price and dividing it by what that same property would fetch in annual rent.

Price to Rent Ratio = Property Price / Annual Rent

A ratio between 1 and 15 indicates that buying is clearly cheaper than renting. Between the ratios of 16 and 21, the cost of buying and renting is comparable, as the decision depends on factors like income stability and length. Above 21, renting is the cheaper option.

Example: Take a property worth ₹80 lakh. The monthly rent on it is ₹22,000.

Annual rent = ₹22,000 x 12 = ₹2,64,000

The ratio works out to:

₹80,00,000 / ₹2,64,000 = 30.3

That places the property well into renting territory.

Now compare this to the cost of buying. A 20% down payment of ₹16,00,000 leaves the loan at ₹64,00,000. The EMI on this amount comes to roughly ₹55,500 for 20 years at 8.5% interest. This is more than double the ₹22,000 rent figure.

This gap narrows over time. At a 7% annual rent increase, the same flat would cost around ₹30,900 a month in rent within 5 years, and ₹43,300 within 10 years, while the EMI stays fixed at ₹55,500 for the full 20-year tenure. As rent climbs, the ratio drops with it, falling to roughly 21.6 within a decade, moving the property from renting territory into a borderline neutral zone.

Tax Benefits of a Home Loan vs Renting

Under the old regime, home loan interest qualifies for a deduction up to ₹2 lakh a year under Section 24(b) of the Income Tax Act, 1961, and principal repayment adds another ₹1.5 lakh under Section 80C. First-time buyers meeting specific conditions (loan sanctioned between April 2019 and March 2022, with a stamp duty value which is equal to or less than ₹45 lakh) can claim an additional ₹1.5 lakh under Section 80EEA. These benefits matter most early on, when interest makes up the bulk of each EMI.

Renters drawing House Rent Allowance (HRA) can claim an exemption under Rule 279 of Income-Tax Rules, 2026, worked out as the smallest of three figures: actual HRA received, rent paid minus 10% of basic salary, or 50% of basic salary in select metros including Delhi, Mumbai, Chennai, Kolkata, Hyderabad, Pune, Ahmedabad, and Bengaluru and 40% elsewhere. Those without HRA fall back on the narrower Section 80GG instead, capped at ₹5,000 per month or 25% of the total annual income.

Switch to the new regime, and none of this applies, neither to home loans nor to rent. At that point, the choice stops being about tax savings and becomes purely about cash flow and long-term goals.

Home Loan vs Rent

Understanding the distinctions between a home loan vs rent across different parameters makes it easier to make a decision.

| Parameter | Home Loan | Renting |

| Monthly outflow | Higher, fixed EMI each month | Lower, but subject to annual hikes |

| Upfront Cost | High, down payment plus stamp duty and registration | Low, security deposit and brokerage |

| Ownership | Full ownership once loan is repaid | No ownership stake built over time |

| Flexibility | Low, tied to one city and property | High, easy to relocate as needed |

| Tax Benefit | Available under old tax regime only | HRA exemption under old tax regime only |

Common Mistakes to Avoid

A handful of errors keep showing up on both sides of the decision between renting and owning.

- Maxing out the EMI: Pushing it to the very edge of what a lender allows leaves no breathing room for anything unplanned.

- Forgetting the extra costs: Stamp duty, registration, interiors. Treating these as afterthoughts almost always leads to a budget shock later.

- Skipping the legal homework: Title verification, encumbrance checks, RERA registration. Skip these, and problems tend to surface years down the line, when they are far harder to fix.

- Letting the rent savings vanish: If renting saves money but that money never gets invested, the entire financial case for renting quietly disappears.

- Putting off the decision endlessly: Waiting without a plan usually just means buying later at a higher price, since most growing cities see values climb each passing year.

- Settling for the first offer: Whether it is a lender or a landlord, not comparing alternatives often means leaving better terms on the table.

Which One Makes More Financial Sense?

The right choice depends on where you are in life, not on which option looks better on paper.

Go for a home loan if:

- You plan is to stay in the same city for a long period, like seven years or more

- Income is stable and the EMI will sit within a comfortable range

- The down payment can be made without depleting emergency savings

- Your goal is to build ownership through disciplined, long-term repayment

Consider renting if:

- Your income is still building toward a stable level

- Making the down payment will stretch your finances thin

- A career move or relocation is a possibility in the near-term

- You will sincerely commit to investing the amount saved from renting

Conclusion

Home loans and rent work on different logics. One builds an asset slowly through fixed monthly commitments; the other keeps money liquid but demands discipline to turn that liquidity into anything lasting. Neither approach is flawed; they simply serve different financial phases of a person’s life. The only way to ascertain your decision is to run the numbers against your own city, income, and timeline rather than following a generic assumption.

FAQs

Can I still get tax benefits on a home loan in 2026?

Only if you choose the old tax regime. Under the new regime, which is now the default, the Section 24b interest deduction and Section 80C principal deduction on a self-occupied property are not available, though a let-out property still allows an interest deduction.

How do rising interest rates affect home loan affordability?

Higher interest rates increase borrowing costs, resulting in larger EMIs or longer loan tenures, which can affect overall affordability and household cash flow.

Can home ownership contribute to long-term wealth creation?

Home ownership can support wealth creation through property appreciation and equity accumulation, though outcomes depend on location, purchase price, and market conditions.

Is a home loan considered good debt?

A home loan is often viewed as productive debt because it finances an asset that may appreciate over time while also providing housing security.

Does inflation favour buying or renting?

Inflation can increase both property prices and rents. The overall impact depends on the pace of property appreciation relative to rent growth and income growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}