Mutual funds are investment funds that collect money from investors to invest into financial assets such as stocks, bonds, and other securities. Over time, mutual fund investment in India has witnessed remarkable growth over time.

A decade ago, people mainly relied on fixed deposits, gold, and real estate. But today, millions of Indians invest in mutual funds through Systematic Investment Plans (SIPs) to build wealth for retirement, children’s education, and other long-term goals.

In May 2026, SIP contributions stood at ₹30,954 crore, and the total mutual fund industry AUM crossed ₹81,58,342 crore, according to the latest data from the Association of Mutual Funds in India (AMFI). Behind this are crores of ordinary Indians, including salaried employees, shopkeepers, homemakers, and young professionals, who are building wealth with one instalment at a time.

The rise of digital investment platforms, growing financial awareness, and easier access to investment products have encouraged more people to start their investment journey.

Yet many first-time investors still have questions! Such as:

What exactly is a mutual fund? How to invest in SIPs as beginners? Should you choose direct or regular plans? Which fund category suits your goals? How are mutual funds taxed?

This complete guide on mutual funds brings together the essential information you need before starting your journey!

Understanding a Mutual Fund & Its Mechanism

A mutual fund is a financial pool created by an investment company that collects money from many individuals to buy a diversified mix of assets such as shares, bonds, government securities, or other market instruments.

Instead of identifying, purchasing, and monitoring individual securities independently, you can participate in a portfolio that is managed according to a predefined investment mandate by professional fund managers. The fund follows a predefined investment objective, which guides how the money is invested and managed over time.

Additionally, when you invest in a mutual fund scheme, you do not directly own the underlying securities held by the fund. Instead, you receive units of the scheme. The value of these units rises or falls based on the performance of the assets held within the portfolio. As the assets within the fund generate gains, you may witness a corresponding increase in the value of their holdings. Conversely, a decline in the value of the underlying assets can reduce the worth of the units held.

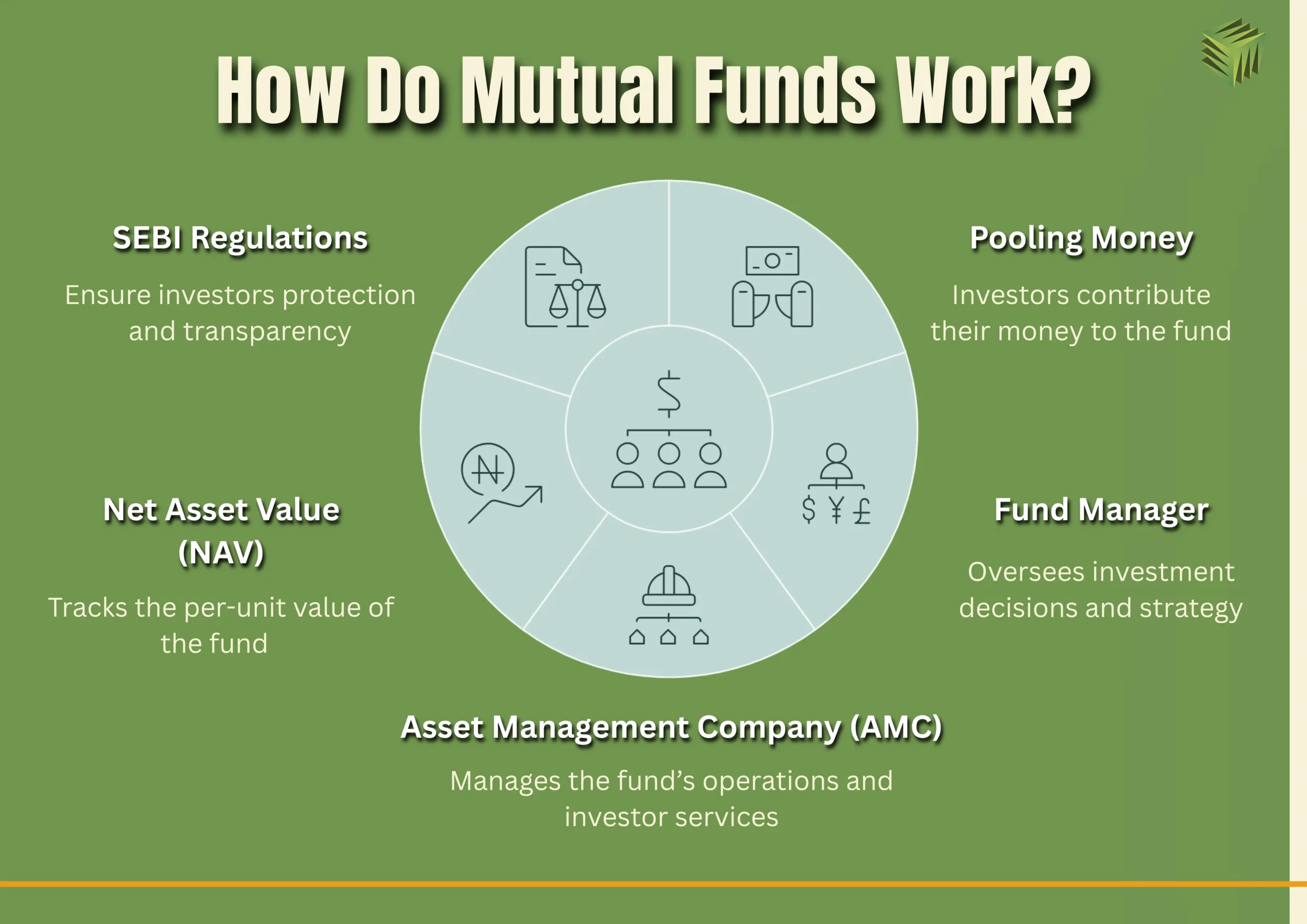

How Do Mutual Funds Work?

The basic principle of a mutual fund is collective investing, where money from many investors is combined and managed as one portfolio. When an investor purchases units of a mutual fund, their money is combined with contributions from other investors and invested according to the scheme’s objective. In exchange for their investment, investors are allotted units that correspond to their stake in the scheme’s assets.

These pooled funds are managed by a fund manager, who decides where the money should be allocated based on the fund’s strategy. These decisions are supported by research analysts and risk management teams that monitor market conditions and investment opportunities.

The overall responsibility for operating the mutual fund rests with an Asset Management Company (AMC). The AMC is responsible for managing the scheme, handling investor services, maintaining compliance, and ensuring that the fund is run according to its stated objective.

The value of each mutual fund unit is reflected through the Net Asset Value (NAV). It represents the per-unit value of a scheme and is calculated by dividing the net value of the fund’s assets, after deducting liabilities and expenses, by the total number of units outstanding. Since the market value of the underlying investments changes regularly, the NAV also fluctuates from one trading day to the next.

The mutual fund industry is supervised by the Securities and Exchange Board of India (SEBI), which prescribes rules relating to disclosures, valuation practices, and investor safeguards. SEBI sets rules relating to disclosures, valuation methods, risk management practices, and investor protection measures. As a result, investors can participate in professionally managed portfolios within a well-defined regulatory framework.

Types of Mutual Funds in India

Mutual funds in India are classified according to the assets they invest in and the financial goals they are designed to serve. These classifications provide a useful framework for selecting funds based on individual financial goals and investment timelines.

According to the categorisation framework prescribed by SEBI and followed by AMFI, mutual funds are divided into equity, debt, hybrid, and solution-oriented schemes. The role played by each category within an investment portfolio differs according to its underlying assets, objectives, and risk profile.

Equity / Debt / Hybrid / Solution-Oriented

Mutual funds in India are classified according to the assets in which they invest. The equity mutual fund segment occupies the largest share of the mutual fund universe and derives its returns primarily from investments in listed stocks. Owing to their equity-oriented nature, these funds are generally associated with higher growth prospects as well as higher volatility, making them more suitable for long-term investors.

In contrast, debt mutual funds build their portfolios around fixed-income assets, where returns are generated primarily through interest income and changes in bond prices. The goal of such funds is to provide moderate growth and income while limiting the sharp fluctuations commonly associated with equity funds.

Between these two categories, we have hybrid mutual funds, which is a combination of growth-oriented and income-oriented assets within one portfolio to diversify risk. By balancing growth-oriented and income-generating assets, hybrid funds attempt to moderate portfolio risk while still participating in market opportunities.

Another category is solution-oriented funds, which are designed around specific financial goals. These investments can help individuals accumulate wealth gradually for important future commitments like retirement and children’s education.

Flexi-Cap vs Multi-Cap vs Large-Cap

Among equity categories, the discussion around flexi-cap vs multi-cap funds has become increasingly common. Although both invest across companies of different sizes, their investment mandates differ.

A flexi-cap fund allows the fund manager to move freely between market-cap segments while maintaining the required equity allocation. This flexibility enables the portfolio to adapt more easily to changing opportunities across the market.

Multi-cap funds are designed to provide balanced participation across different company sizes within the equity market. This creates wide market participation but also limits the fund manager’s flexibility to significantly alter allocations when market conditions change.

A large-cap fund, on the other hand, invests predominantly in India’s largest listed companies. These businesses are generally well-established and tend to experience relatively lower volatility than smaller companies.

ELSS Tax-Saving Funds

Equity Linked Savings Schemes (ELSS) occupy a unique position within the mutual fund universe. These are equity-oriented mutual funds that qualify for Section 80C tax deductions of up to ₹1.50 lakhs under the Income Tax Act, subject to prevailing tax rules.

Unlike many traditional tax-saving products, ELSS funds invest predominantly in equities while carrying a mandatory three-year lock-in period.

Since they combine market-linked growth potential with tax benefits, ELSS funds are often considered by investors who want to build long-term wealth while reducing their taxable income. Their role within a portfolio, however, should be evaluated alongside other tax-saving options rather than viewed solely as a tax-planning tool.

What to choose: Direct vs Regular Mutual Funds

After choosing a mutual fund category, the next decision is equally important: whether to invest through a direct plan or a regular plan. The debate around direct vs regular mutual funds starts at this point. Despite investing in the same scheme, investors may encounter different fee levels and support structures.

A direct mutual fund enables investors to deal directly with the fund house, bypassing commission-based distribution networks. The absence of distributor commissions often results in lower ongoing costs for direct plans.

A regular mutual fund is purchased through distributors, brokers, banks, or financial advisers. In this case, the AMC pays a commission to the intermediary, and this cost becomes part of the scheme’s expense ratio. As a result, regular plans typically have slightly higher annual expenses than their direct counterparts.

| Feature | Direct Mutual Funds | Regular Mutual Funds |

| Purchase Route | Here you can invest in a mutual fund directly through the AMC. | Here you can invest through a broker, distributor, bank, or financial advisor. |

| Intermediaries | None. | Yes; you pay for the distributor’s or broker’s services. |

| Expense Ratio | Lower (excludes commission costs). | Higher (includes commission deducted from your investment). |

| Returns / NAV | Yields higher overall returns in the long run due to the lack of deducted fees. | Yields lower returns because a portion of the fund value goes to distributor commissions. |

| Suitability | Works well for investors who conduct their own research and make investment decisions independently. | Best for beginners or investors wanting ongoing advisory, portfolio reviews, and assistance with paperwork. |

| Advisory & Support | Self-managed; you track your own goals and market shifts. | Advisory provided; the distributor helps choose funds and monitors your portfolio. |

For further breakdown, read our detailed guide on Direct vs Regular Mutual Funds – Which Is Better?

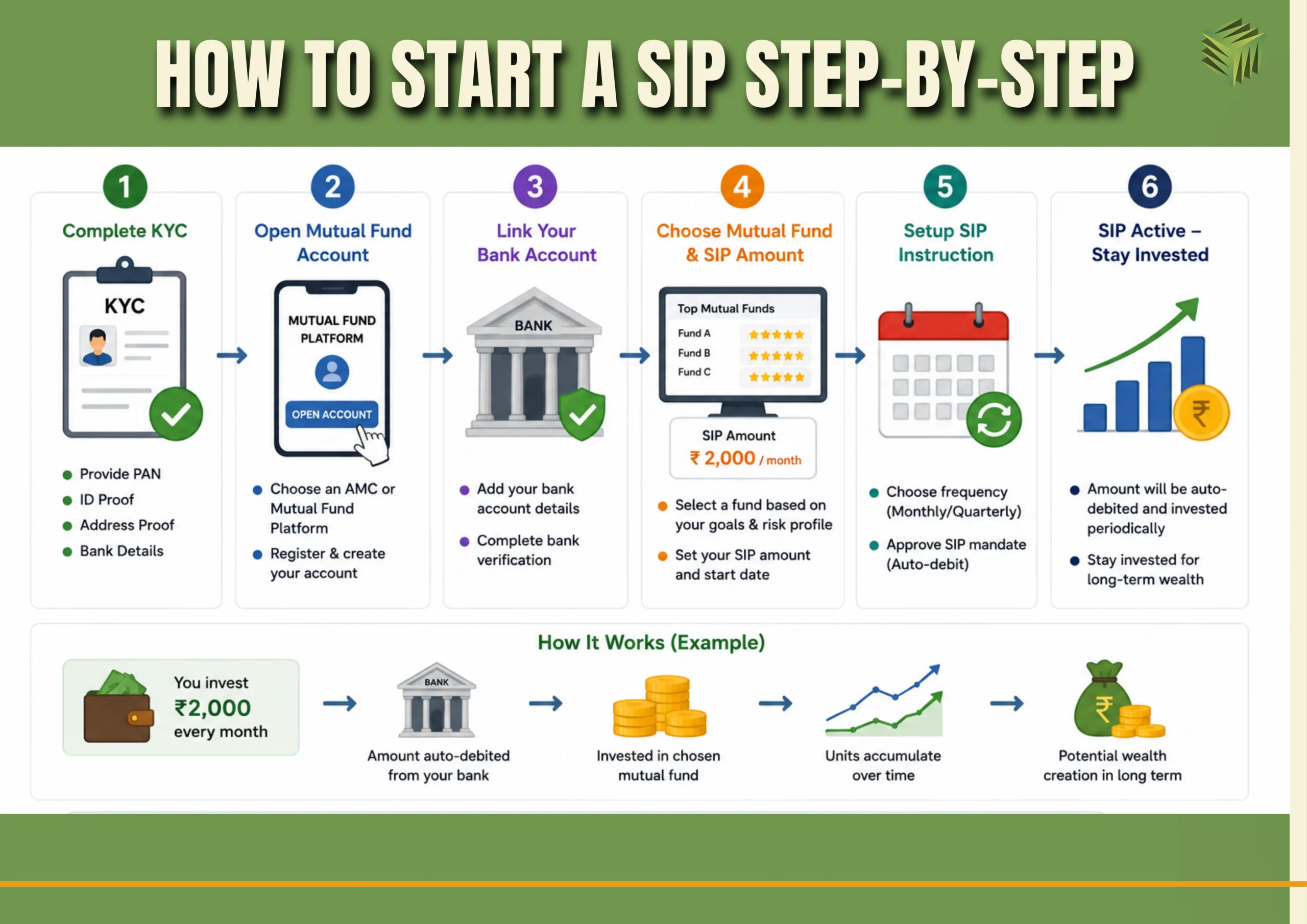

How to Start a SIP Step-by-Step

Once a suitable mutual fund category and investment plan are selected, the next step is setting up a Systematic Investment Plan (SIP). With a SIP, investors can invest a chosen amount periodically, helping build an investment habit over time.

The following steps help you understand how to start an SIP investment as a beginner:

KYC & Account Setup

Completing KYC verification is one of the first steps for anyone planning to invest in mutual funds. This verification process strengthens investor identification and supports regulatory compliance requirements. Applicants typically need to submit PAN information, identity documents, and bank account particulars as part of the KYC procedure.

Once KYC verification is completed, you can open an account through an AMC website or a mutual fund investment platform. And, after linking a bank account, you can start purchasing mutual fund units and setting up SIP instructions.

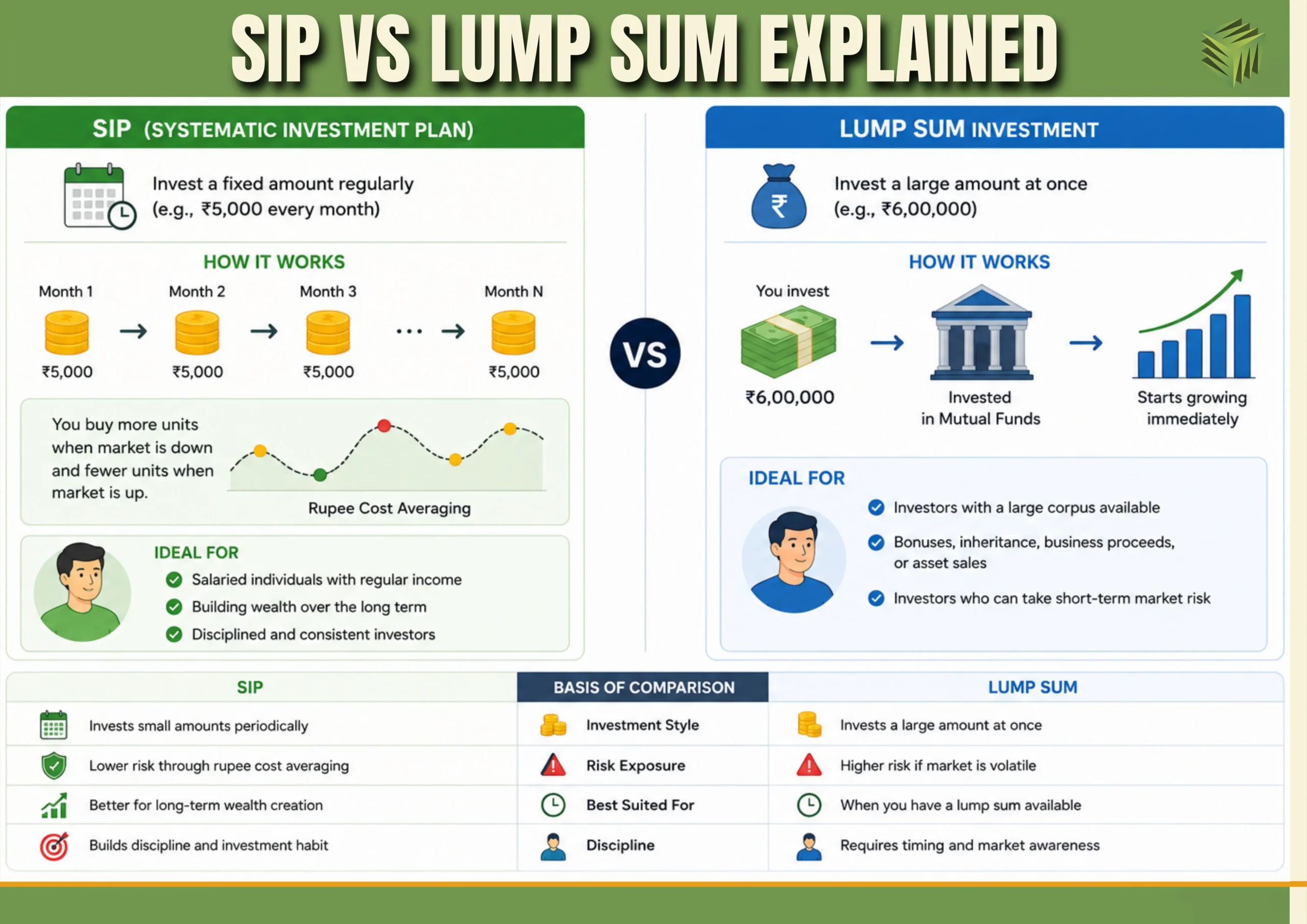

SIP vs Lump Sum Explained

SIP vs lump sum investing is another common debate while investing in mutual funds. Both approaches can help build wealth, but the right choice depends on income patterns, market conditions, and investment objectives.

A SIP follows a scheduled investment pattern, allowing investors to accumulate units under varying market conditions. While a lump sum investment, on the other hand, puts the entire amount to work immediately. It is generally considered when an investor has a large sum available for investment.

If you are a salaried individual with regular income, SIPs could be a more practical and disciplined approach. Lump sum investing is more commonly used when funds become available through bonuses, business proceeds, inheritance, or asset sales.

Best Platforms (Coin, Groww, MF Central)

Investors searching for the best SIP plans in India should focus on selecting funds that align with their financial goals, investment horizon, and risk tolerance rather than choosing schemes solely based on recent returns. Today, investors can start SIPs through several digital platforms. A few popular platforms are:

- Coin by Zerodha: It allows you to purchase direct mutual funds through a demat-linked account.

- Groww: The platform offers a simple investment experience along with tools to monitor mutual fund holdings.

- MF Central: It is an industry-backed platform developed to offer a centralised service portal for mutual fund investors.

Once you have decided on a platform, you can choose a fund, specify the SIP amount, select the investment date, and authorise automatic bank debits. When it gets activated, the SIP continues until modified or cancelled by the investor.

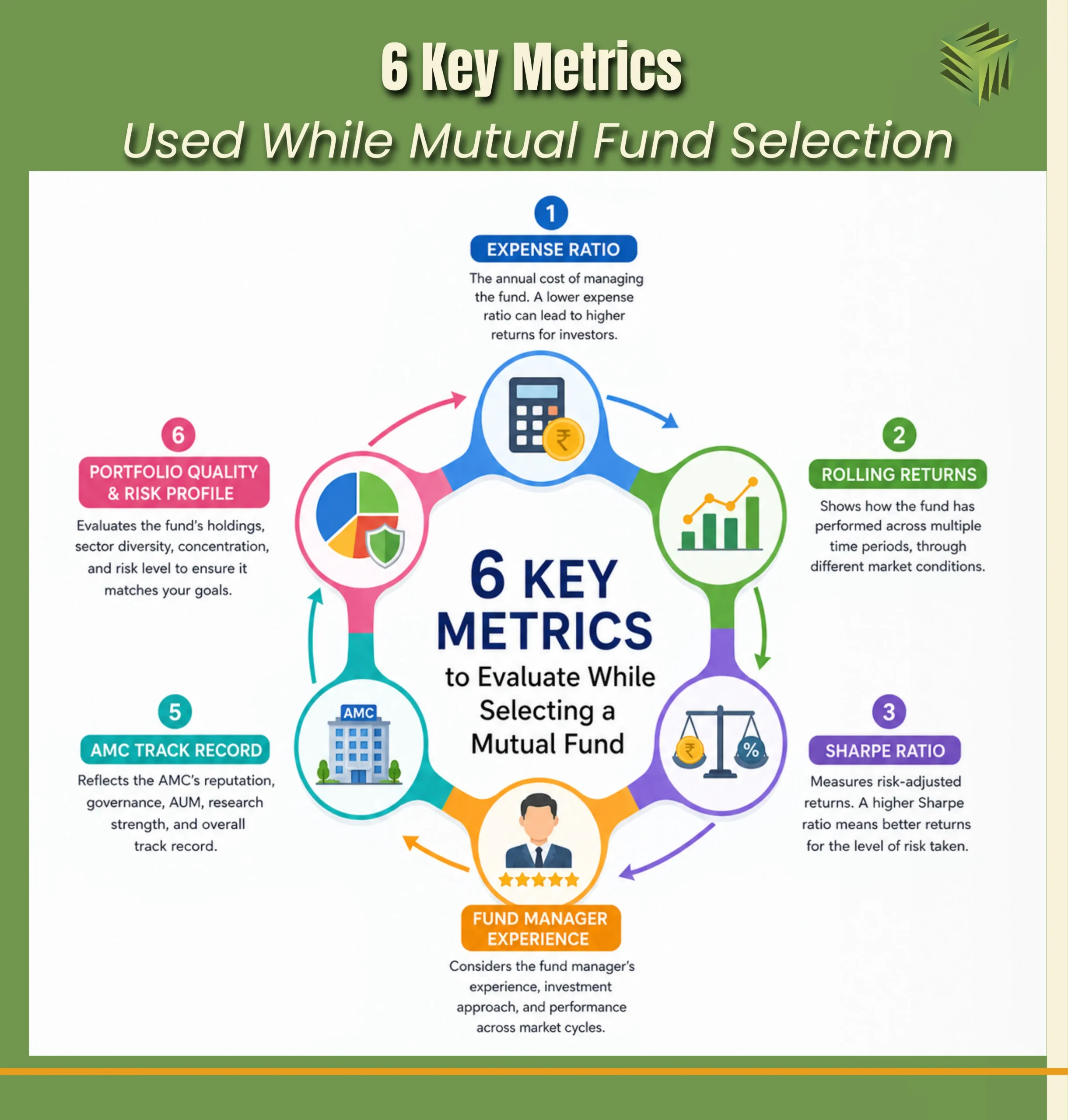

6 Key Metrics Used While Mutual Fund Selection

The large number of mutual fund schemes in the market can make the selection process more complex for investors. Rather than focusing solely on recent returns, investors should evaluate a combination of performance, risk, cost, and fund management factors before making a decision.

Here are 6 key metrics you should evaluate while selecting a mutual fund:

- Expense Ratio

The expense ratio reflects the yearly cost deducted by a mutual fund to cover fund management and operating expenses. It covers portfolio management, administrative expenses, and operational costs. Since this fee is deducted from the fund’s assets, a lower expense ratio can leave a larger portion of returns in the hands of investors. According to the Association of Mutual Funds in India (AMFI), expense ratios vary across fund categories and between direct and regular plans.

- Rolling Returns

Rolling return analysis considers numerous investment windows to present a more balanced view of historical results. It provides a wider assessment by measuring returns across multiple overlapping periods. It helps determine whether a fund has maintained a consistent track record under different market circumstances rather than benefiting from one exceptional period.

- Sharpe Ratio

The returns of a mutual fund alone do not reveal the level of risk undertaken to achieve them. The Sharpe ratio measures risk-adjusted performance by comparing a fund’s excess return with the volatility experienced along the way. In this regard, a higher Sharpe ratio generally indicates that investors were compensated more efficiently for the level of risk assumed.

- Fund Manager Experience

A mutual fund’s performance is influenced by the investment decisions made by its fund manager and supporting research team. Reviewing a manager’s tenure, investment philosophy, and track record across different market cycles can provide useful insights into the consistency of the investment process.

- AMC Track Record

The reputation and governance standards of the Asset Management Company (AMC) also deserve attention. Well-established AMCs often possess extensive research resources, mature risk controls, and proven operational frameworks. You should review the AMC’s history, assets under management, and overall track record before investing.

- Portfolio Quality and Risk Profile

A fund’s portfolio reveals where investor money is actually being invested. Reviewing sector allocations, major holdings, diversification levels, and risk indicators can help determine whether the scheme aligns with an investor’s objectives and risk tolerance.

If you want to analyse mutual fund portfolios, track market trends, and access advanced stock research tools, you may also explore online platforms. The platform offers market data, screening tools, and research features that can support informed investment decisions.

How to Read a Fund Factsheet

Most of the information discussed above can be found in a mutual fund factsheet. These monthly reports typically include portfolio holdings, fund manager details, sector allocation, risk measures, expense ratio, and historical performance data. By learning how to read a factsheet, you can move beyond marketing claims and make decisions based on actual fund characteristics.

What Happens When a Fund Manager Leaves?

Now, in mutual fund investments, a fund manager plays a very significant role in security selection and portfolio construction, but a mutual fund does not depend on a single individual, just like a mutual fund does not depend on a single security.

Most schemes operate within a defined investment framework supported by research analysts, risk management teams, and investment committees. Consequently, when a fund manager leaves the AMC, it does not automatically alter the fund’s objective or investment process.

However, investors should review the new manager’s experience, investment style, and any changes in portfolio strategy over the following months.

Taxation of Mutual Funds in India (2026)

Mutual fund taxation is generally based on two key factors: the category of the fund and the holding duration. Under the updated tax framework, equity-oriented funds and specified mutual funds are subject to different taxation provisions. You should, therefore, evaluate post-tax returns rather than focusing solely on fund performance.

| Equity-oriented Mutuals Funds | ||

| Tax Status of Investor | Capital Gains Tax | |

| Short-term | Long-term | |

| Individual Investors | 20% (<12 Months) | 12.5%, with no indexation (>12 Months) |

| Specified Mutuals Funds | ||

| Tax Status of Investor | Capital Gains Tax | |

| Short-term | Long-term | |

| Individual Investors | Investments made before 1 April 2023 and redeemed by 23 July 2024 after being held for under 24 months: at applicable income tax slab rate applies | Investments made before 1 April 2023 and redeemed by 23 July 2024 after being held for over 24 months: 12.5% tax rate applies, with no indexation benefit available |

| Bought on or after 1 April:

Taxable at applicable slab, regardless of holding period |

||

ELSS vs PPF vs NPS

In regard to tax planning, investors are usually led to compare ELSS vs PPF vs NPS, three of the most widely used tax-saving investment options in India. Although all three can help reduce taxable income under applicable provisions of the Income Tax Act, they differ significantly in terms of risk, lock-in period, liquidity, and return potential.

An ELSS is a tax-saving mutual fund that allocates most of its corpus to equities. Investors can claim deductions under Section 80C, subject to a mandatory three-year holding requirement. However, since ELSS funds are market-linked, the returns are not guaranteed and can fluctuate with market conditions.

Public Provident Fund (PPF) is a long-term savings vehicle backed by the Government of India and aimed at gradual wealth creation. It offers a longer lock-in period of 15 years but is generally preferred by conservative investors seeking stability and sovereign backing. Similar to ELSS, PPF also offers ₹1.50 lakhs deductions under Section 80C. Additionally, it enjoys the EEE (Exempt-Exempt-Exempt) tax status under the current tax framework.

The National Pension System (NPS) offers Section 80C benefits and may also qualify for an additional deduction under Section 80CCD(1B), subject to applicable tax rules. This additional tax benefit is one of the key reasons NPS is frequently considered by investors building a retirement corpus.

The choice between ELSS, PPF, and NPS should depend on an investor’s financial goals, investment horizon, risk tolerance, and liquidity requirements rather than tax benefits alone. Investors seeking long-term market participation may prefer ELSS, while those prioritising capital preservation or retirement planning may find PPF or NPS more suitable.

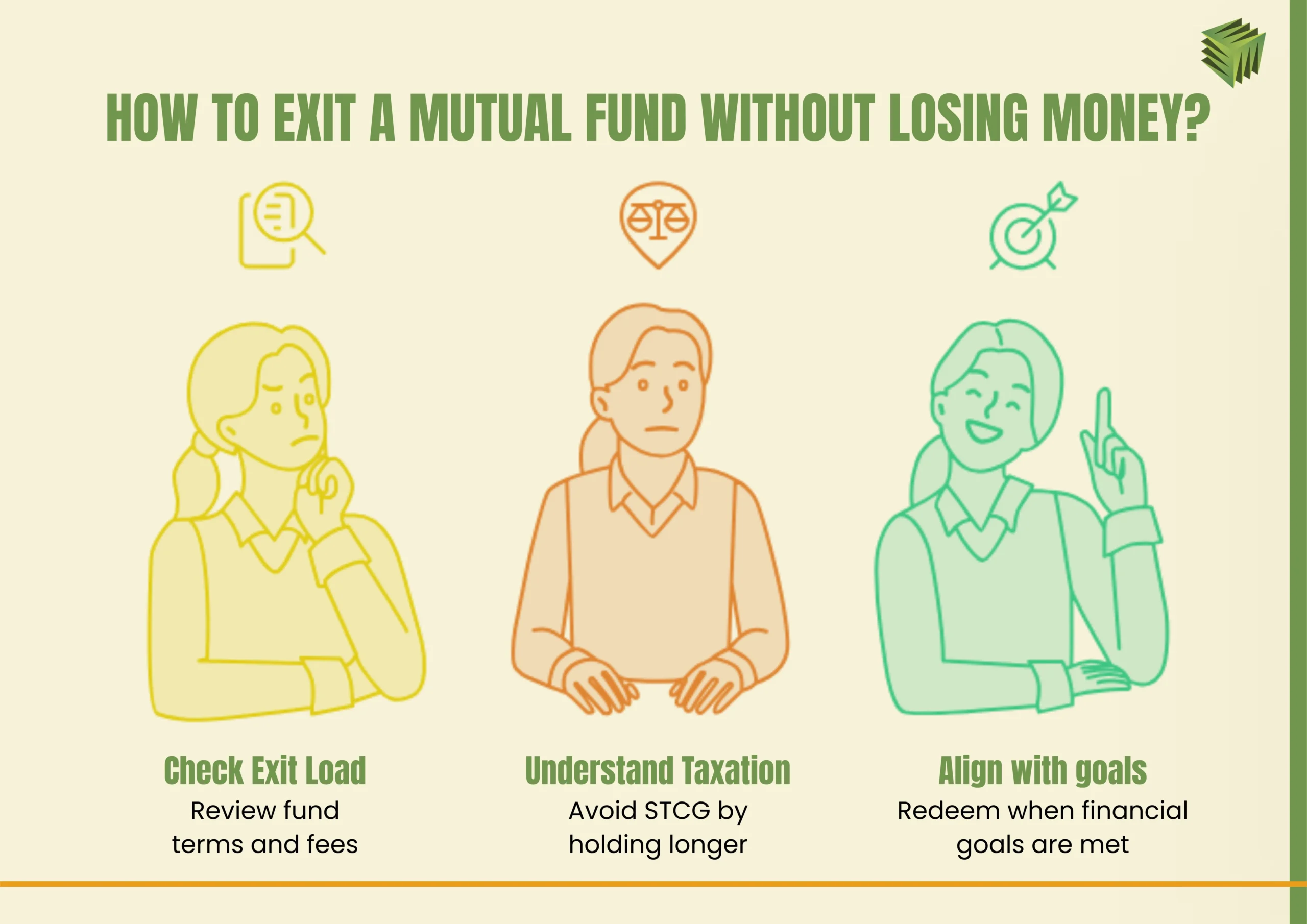

How to Exit a Mutual Fund Without Losing Money

While investing is one half of the journey, knowing when and how to exit a mutual fund without making a loss is equally important. An unplanned redemption can reduce returns through taxes, charges, or poor timing.

One of the first things to check is the mutual fund exit load schemes that may charge for early redemption. An exit load refers to a fee charged on premature withdrawals from a mutual fund, depending on the fund’s terms and conditions. Since the charge varies across schemes, investors should review the fund’s terms before redeeming.

Taxation is another important consideration. Selling units before qualifying for long-term capital gains treatment may trigger Short-Term Capital Gains (STCG) tax, which can reduce overall returns. Reviewing the tax implications before redemption can help investors avoid unnecessary costs.

In most cases, mutual funds should be redeemed when the intended financial goal has been achieved, the fund no longer suits the investor’s risk profile, or there has been consistent underperformance. As explained in the Exit Strategy Guide, redemption decisions should be driven by financial objectives rather than short-term market movements.

Picking Mutual Funds for Specific Goals

A mutual fund should be selected based on the purpose it is expected to serve. An emergency fund, a retirement corpus, and a child’s university education may all involve investing money, but they have very different timelines and requirements. And, choosing the wrong type of fund for the wrong goal can create unnecessary risk at the very moment the money is needed.

For long-term objectives such as retirement planning, investors often consider equity-oriented funds because they offer greater growth potential over extended periods. Since retirement goals may be decades away, investors generally have more time to ride out short-term market fluctuations.

An emergency corpus, on the other hand, prioritises quick accessibility and safeguarding capital rather than generating higher returns. Since the money may be needed at short notice, investors typically prefer low-risk options such as liquid funds or other short-duration debt-oriented schemes. According to the AMFI, investment choices should align with the purpose and time horizon of the goal being funded.

Child’s Education Planning

Similarly, planning for a child’s education requires balancing growth with certainty. Education costs have risen steadily over the years, making long-term planning increasingly important for parents. Investors looking for a mutual fund for child education in India should consider the number of years remaining before the funds will be required.

Biggest Mutual Fund Mistakes Beginners Make

Many mutual fund investing mistakes arise from investor behaviour rather than fund selection. The following mistakes can hinder investment success and are best avoided:

- Chasing Recent Returns: Many investors invest in funds after a period of strong performance, assuming the same returns will continue. Although past performance provides insight into a fund’s track record, future outcomes may differ considerably because market conditions and leadership trends evolve.

- Stopping SIPs During Market Dips: Market corrections can create uncertainty, but discontinuing SIPs during such periods may limit the benefits of long-term investing. Remaining consistent during market declines supports systematic accumulation at lower entry levels.

- Over-Diversification: Adding too many schemes to a portfolio can lead to repeated investments in similar securities without providing meaningful diversification. A well-selected portfolio does not necessarily require a large number of schemes.

- Ignoring Financial Goals: Investments made without a clear objective often lead to unnecessary switching and inconsistent decisions. The purpose of an investment and the intended holding period should play a central role in mutual fund selection.

- Reacting to Short-Term Market Movements: Frequent investment decisions based on daily market fluctuations can disrupt a long-term strategy. Long-term investment success is frequently associated with staying committed to financial goals despite short-term market volatility.

Bottomline

A successful mutual fund investment is not about finding the highest-returning scheme. It is about selecting suitable funds, understanding costs and taxes, and staying invested long enough for compounding to work.

Whether you invest through SIPs or lump sum contributions, the most effective strategy is one that aligns with your financial goals, risk appetite, and investment timeline. Consistency and informed decision-making are what matter more than market timing.

Frequently Asked Questions

Can I invest in mutual funds without a demat account?

Yes. Most mutual funds can be purchased directly through Asset Management Companies (AMCs), registrar platforms, or online investment platforms without opening a demat account. A demat account is optional for most mutual fund investors.

Is it possible to pause a SIP temporarily?

Yes. Many mutual fund platforms and AMCs allow investors to pause SIP contributions for a specified period. Existing investments continue to stay invested, while future instalments are temporarily suspended.

Can NRIs invest in Indian mutual funds?

Yes. Non-Resident Indians (NRIs) can invest in Indian mutual funds after completing the applicable KYC requirements and complying with relevant banking and regulatory guidelines.

Are mutual funds safer than individual stocks?

Mutual funds generally offer greater diversification because they invest across multiple securities rather than a single company. While they may reduce company-specific risk, they are still subject to market and investment risks.

Can I hold mutual funds jointly with family members?

Yes. Mutual fund investments can be held jointly with family members or other individuals. The rights and transaction rules depend on the mode of holding selected during account registration.

What is a folio number?

A folio number is a unique reference number assigned by an AMC to an investor. It helps track mutual fund holdings, transactions, and account-related information within that fund house.

Can I switch between mutual fund schemes?

Yes. Investors can switch from one scheme to another within the same AMC. However, such transactions may attract taxation and exit load charges depending on the scheme and holding period.

What happens if my bank account changes?

Investors should update their bank details with the AMC or investment platform as soon as possible. This helps ensure that future investments, redemptions, and dividend payments are processed correctly.

Can minors invest in mutual funds?

Yes. Mutual funds can be purchased in the name of a minor through a parent or legal guardian. Once the minor attains adulthood, the account must be updated according to the AMC’s procedures.

How often should I review my mutual fund portfolio?

Reviewing a mutual fund portfolio once or twice a year is usually sufficient. Additional reviews may be necessary if there are significant changes in financial goals, risk tolerance, or market conditions.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}